Anthony Licciardello | May 2, 2026

Long Beach Island

Most "LBI rental income" content gives you peak-week rates and stops there. That's not how an investor actually underwrites a property. Peak-week rates are the headline, but they're the smallest part of the math. The real questions are how many weeks actually book, what the cost stack does to gross income, how the new municipal registration frameworks affect operations, and whether the absolute basis on the property even allows the rental income to matter.

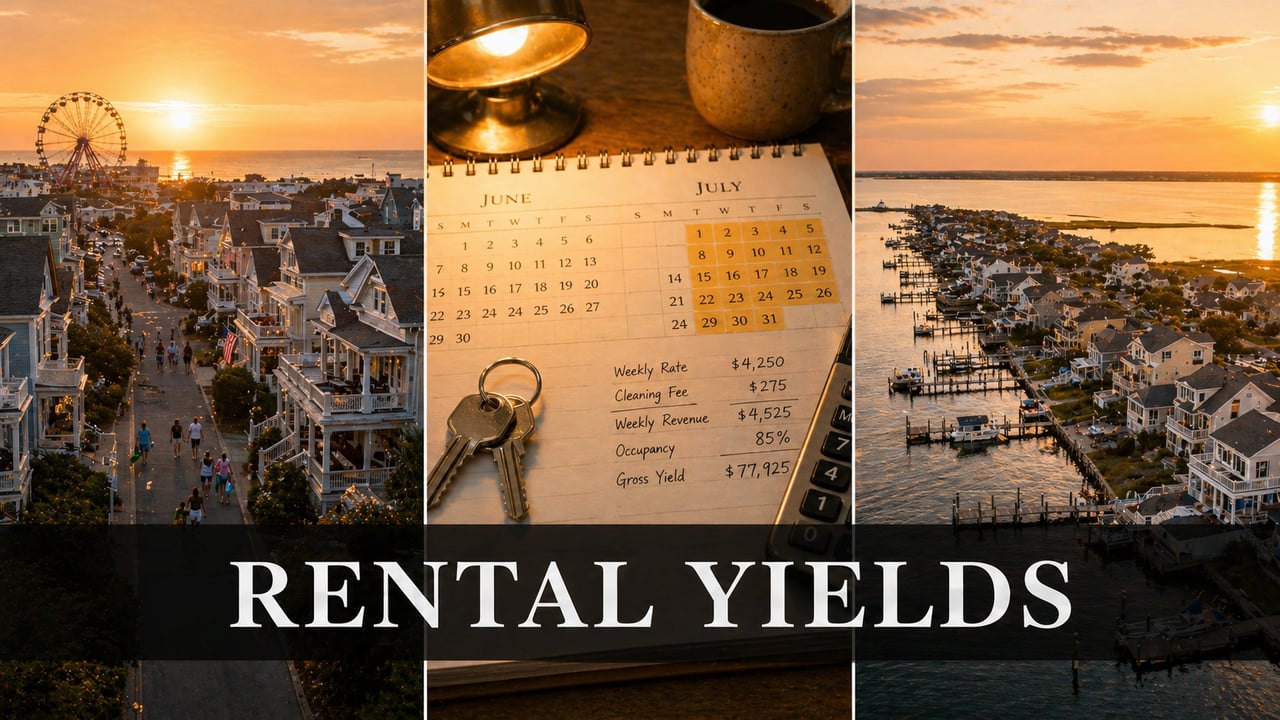

A typical $2 million LBI bayfront with 11 booked summer weeks at an average $7,500/week generates roughly $82,500 gross. After NJ state taxes (where applicable), property management commission, cleaning turnover costs, insurance, property taxes, utilities, and a maintenance reserve, the realistic net cap rate runs 1.5% to 3% on most LBI inventory in 2026. That's well below mainland NJ multifamily yields and below most other shore market alternatives.

But that net yield isn't the whole investor case. LBI buyers who underwrite for blended return — modest current yield plus structural appreciation against a non-replicable barrier-island supply constraint — see materially better total returns than the headline cap rate suggests. The trick is buying in the towns where the yield piece actually shows up in the math, not the trophy enclaves where appreciation does all the heavy lifting.

The LBI rental year has three distinct phases. Peak season runs Memorial Day weekend through Labor Day weekend — roughly 14 weeks of meaningful demand, with the strongest weeks concentrated in mid-June through mid-August. Shoulder season covers mid-May, the first three weeks of September, and parts of October — limited bookings at materially lower rates, often 40 to 60% off peak. Off-season is November through April, when most LBI vacation inventory produces little or no rental income.

The Saturday-to-Saturday weekly booking format is the LBI tradition. Most agencies and direct-rental owners run on this calendar, which simplifies turnover but eliminates the higher per-night yield that nightly Airbnb-style booking can produce in markets with shorter average stays. The trade-off favors operational simplicity and tenant continuity over yield maximization.

A well-marketed, well-located LBI property realistically books 11 to 13 of the 14 peak weeks. Lesser-positioned properties — Boulevard-fronting parcels, dated interiors, small lots without parking — book 7 to 9. Properties in the apex enclaves with strong repeat tenant relationships routinely sell out the entire season by February, but those tend to be the lowest-yield properties on a per-dollar basis because the absolute weekly rate doesn't scale with the acquisition cost.

LBI rental rates are driven by three different premium structures, and they don't all flow through to investor yield equally.

The walkability premium is the strongest yield-driver on the island. Beach Haven leads. Tourists who can park their car for the week and walk to dinner, the boardwalk, Fantasy Island, and Bay Village pay materially more per week than tenants who have to drive to every meal. That premium translates directly into stronger weekly rates and stronger booking velocity, while acquisition basis remains below the northern apex.

The beach-quality premium shows up most clearly in Surf City, where federally funded replenishment has produced some of the widest sand on the island. Wider beaches translate to higher tenant satisfaction, stronger repeat bookings, and modestly higher weekly rates. The yield impact is real but smaller than the walkability premium.

The privacy and prestige premium commands the highest absolute weekly rates on the largest properties — Loveladies, North Beach, and to a lesser extent Harvey Cedars. But on a yield basis, the premium pricing rarely covers the higher acquisition basis. A $5 million Loveladies oceanfront might command $30,000 a week peak. That's a remarkable absolute number, but on a $5 million basis, it's a smaller percentage of property value than a $2 million Beach Haven oceanblock at $12,000 a week. Trophy assets produce trophy revenue. They don't necessarily produce trophy yield.

For yield-focused investors, the takeaway is direct: the highest-rate town isn't the highest-yield town. The framework set out in the LBI town-by-town real estate guide for buyers also applies to investors — but inverted, because the towns that command the highest sale-price premiums often deliver the lowest rental yield premiums.

Beach Haven consistently produces the strongest rental yields on the island for one reason: walkability. The dense Victorian-era street grid puts tenants within walking distance of restaurants, the boardwalk, Fantasy Island Amusement Park, Bay Village, and Surflight Theatre. Renters pay more, and they book more weeks.

Current 2026 weekly rate ranges, drawn from active LBI listing platforms:

A well-positioned 5-bedroom Beach Haven oceanblock at $9,500 average weekly rate, booking 12 of 14 peak weeks, generates approximately $114,000 gross. On a $2 million acquisition basis, that's a 5.7% gross-rate-of-return — before any costs. The acquisition basis matters as much as the rental income; Beach Haven's pricing tier sits below the northern apex while the rental rates remain competitive, which is what makes the yield math work.

The trade-offs: density, summer congestion, lower privacy, and the highest summer noise levels on the island. For an investor, none of those are problems. They're features. They're what produces the rental yield premium.

Surf City sits in the second-strongest yield tier. Walkable Boulevard commercial, federally replenished beaches that are among the widest on the island, and a balanced rate structure that benefits from both walkability and beach quality. Current 4-bedroom oceanside ranges run $2,800–$8,500/week; 5-bedroom larger properties reach $4,725–$16,450/week. Oceanfront in Surf City typically commands $12,000–$20,000/week peak.

Ship Bottom produces a different yield equation. The town's gateway commercial density and causeway proximity create the fastest sale liquidity on the island, but per-week rental rates run lower than Surf City for comparable square footage because the commercial noise and traffic suppress weekly rates. A typical 3-bedroom Ship Bottom property starts at $4,300/week. The yield case in Ship Bottom rests on a meaningfully lower acquisition basis than the rest of the island, which can produce competitive cap rates even with lower absolute rents.

For cash-flow-focused investors entering LBI, Ship Bottom often produces the cleanest math: lower entry, faster exit liquidity if needed, and rental rates that — while not at the top of the island — still benefit from the structural LBI summer demand pattern. A new 2025 Ship Bottom rental ordinance proposal added some operational complexity that owners should verify before underwriting, but the underlying yield case remains intact.

Long Beach Township covers more rental inventory than any other LBI municipality by parcel count. The mid-island stretch — Brant Beach, Beach Haven Crest, Brighton Beach, Peahala Park, Beach Haven Park, Beach Haven Gardens, Spray Beach, North Beach Haven, Haven Beach, The Dunes — is where most LBI rental investors actually own. Standard 50x100 lots, mixed building stock from older Cape Cods to 2024 modern reverse-living new construction, and per-square-foot pricing tracking near the islandwide average.

Brant Beach is the volume-tier representative. Current 2026 weekly rate examples include 5-bedroom oceanblock properties listing at $12,750–$15,750/week and oceanside 3-4 bedroom homes in the $4,500–$8,500/week range depending on proximity to the beach and condition. Brighton Beach 3-bedroom oceanside properties run more modest rates — often $2,500–$4,500/week. Bayside parcels across the LBT mid-island typically rent for 25 to 40% less than oceanblock equivalents.

The yield case for the LBT mid-island rests on three things: lower acquisition basis than Beach Haven or the apex enclaves, comparable rental rates to Surf City on equivalent product, and the fact that this band represents the highest-volume rental investor activity on the island — meaning a deeper pool of comparable transactions to underwrite against. The annual Long Beach Township rental property registration framework, with applications due no later than April 1st each year, is now in its second cycle as of 2026, and late filing penalties apply for non-compliance.

The northern apex enclaves command the highest absolute weekly rental rates on the island. Current Loveladies oceanside 4-bedroom listings range $7,500–$13,500/week. Harvey Cedars 6-bedroom homes list $9,950–$10,950/week and reach significantly higher on oceanfront product. North Beach commands premium rates similar to Loveladies. These are real numbers and meaningful gross income.

The yield problem is the denominator. Weekly rental rates do not scale 1:1 with property values. A $5 million Loveladies oceanfront commanding $30,000 per week peak is generating about 0.6% of property value per peak week, while a $2 million Beach Haven oceanblock at $12,000 per week is generating 0.6% as well — but the Beach Haven property has smaller carrying costs, lower property tax exposure on the smaller basis, and a meaningfully lower opportunity cost of capital tied up in the asset.

Loveladies and North Beach buyers are mostly trophy-asset buyers, not yield-focused investors. The rental income subsidizes carrying costs rather than generating cash flow. For these buyers, the rental program is an offset against tax liability and ownership expense, not a return-on-investment driver. The structural appreciation — driven by 100x100 lot sizes, private lane beach access, and absolute commercial-zoning absence — does the heavy lifting on total return. The cap rate math, taken in isolation, doesn't work.

Harvey Cedars is the closest the northern apex gets to a yield play. Modern post-2019 construction commands premium weekly rates, the standard 50x100 lot footprint keeps the acquisition basis below Loveladies, and the high-elevation dune system and structural resilience profile produce competitive insurance economics. For investors targeting the upper tier of LBI rental, Harvey Cedars is the cleanest math.

The gross rental number is the easy part. Here's what the cost stack does to it on a typical $2 million LBI rental property generating $80,000 gross.

Property management commission: 10% is the LBI standard, paid from rental checks. Major LBI brokerages including Van Dyk Group operate at this rate, which is meaningfully lower than the 23 to 28% national average for full-service vacation rental management. The reason is structural — LBI uses the licensed-real-estate-broker rental model rather than the full-service vacation management model, which means the rental program operates as a brokerage transaction rather than a hospitality service. On $80,000 gross, that's $8,000.

NJ state taxes: 6.625% sales tax + 5% state occupancy fee = 11.625% baseline, applied to bookings made through transient marketplaces (Airbnb, VRBO) or by owners with 3+ NJ rental units. Direct owner bookings of fewer than 3 units, and bookings handled through licensed real estate brokers with key delivery at the broker's office, are exempt. The marketplace exemption is meaningful — direct-booked LBI rentals avoid the entire state tax stack. Most LBI investors use the licensed-broker model specifically to preserve this exemption.

Property taxes: Vary by municipality, but a $2 million LBI bayfront typically pays $18,000–$28,000 per year in property tax depending on town and assessed valuation.

Insurance: Elevated on LBI due to flood exposure. Standard NFIP coverage plus wind/hazard runs $5,000–$15,000+ per year on a typical bayfront, with private flood market alternatives sometimes reducing the total. Oceanfront and high-flood-zone parcels run higher.

Cleaning fees per turnover: $300–$700, often passed through to tenants but eats margin if not.

Utilities, lawn, pool maintenance: $5,000–$12,000/year typical.

Municipal STR registration: Long Beach Township requires annual registration with applications due April 1st. Other LBI municipalities (Beach Haven, Surf City, Ship Bottom, Harvey Cedars, Barnegat Light) maintain their own rental ordinance frameworks, fees, and inspection requirements. Verify the specific town's 2026 framework before underwriting.

Maintenance reserve: 1–2% of property value annually. On a $2 million property, that's $20,000–$40,000/year for long-term capital expenditure (HVAC replacement, roof, decks, bulkhead — see the LBI bulkhead question for the bayfront-specific reality).

A $2M LBI bayfront earning $80K gross with 10% management, $22K property tax, $9K insurance, $7K utilities/maintenance, $20K reserve, and minimal direct-booking tax exposure produces roughly $14K–$16K net. That's a 0.7–0.8% net cap rate. Add $40K–$80K in annual property appreciation against the $2M basis, and the blended return reaches 2.7–4.8% — which is the actual investor return on LBI rental, not the headline cap rate.

LBI rental investments make sense if you're underwriting for blended appreciation plus partial yield, you're targeting Beach Haven walkability where the yield premium is highest, you can self-manage to compress the cost stack, you're willing to use the property 4–6 weeks personally and rent the balance, you've structured booking through a licensed real estate broker to preserve the NJ state tax exemption, or you're buying with a long enough holding period (10+ years) that structural appreciation against fixed island supply does the work cap rate can't.

LBI rental investments don't make sense if you need pure cash flow to service debt or meet income needs, you're underwriting against mainland NJ multifamily yields (4–7% is normal there and unreachable on LBI), you're buying ultra-luxury in Loveladies or North Beach and expecting yield to justify the price, or you're planning a 3–5 year hold where appreciation hasn't had time to compound.

The honest read: LBI is a luxury second-home market that produces meaningful but secondary rental income. It's not a rental-yield market in the way the Pocono Mountains or upstate New York short-term rental markets are. Underwriting LBI as a yield play produces disappointment. Underwriting it as an appreciation-plus-partial-yield play, with eyes open to the cost stack and the right town selection, produces the actual returns the market generates.

The LBI rental yield map favors mid-island, walkable, and right-sized properties — not the apex enclaves where appreciation does the heavy lifting on total return. For yield-focused investors, Beach Haven leads on walkability premium. Brant Beach and Surf City offer mid-tier balance. Ship Bottom delivers liquidity-plus-yield at the lowest acquisition basis. For ultra-luxury buyers, the rental income subsidizes carrying costs rather than driving return on investment.

The 2025 mansion tax overhaul covered in the LBI closing costs reality meaningfully changed the seller-side math on exit, which directly affects the appreciation piece of the blended-return calculation. The structural supply argument detailed in the oceanfront vs. bayfront 2026 analysis is what makes LBI's appreciation curve work despite a low headline cap rate. And the broader market context lives in the 2026 LBI market report.

For investors entering LBI in 2026, the disciplined move is to model both pieces — yield and appreciation — to a 10-year horizon, then choose the town whose buyer-match framework aligns with the strategy. The headline cap rate doesn't tell the story. The blended return does.

Sources: Current 2026 weekly rental rate data drawn from active listings on Vacation Rentals LBI (vacationrentalslbi.com) and Shore Summer Rentals (shoresummerrentals.com) as of April 2026. Property management commission rate (10%) per Van Dyk Group LBI Rental Services published rate structure. NJ state tax framework (6.625% sales tax, 5% state occupancy fee, marketplace exemptions) per New Jersey Division of Taxation Transient Accommodations guidance and post-2019 legislative amendments. Long Beach Township annual rental registration framework per Township Municipal Clerk's Office (longbeachtownship.com). Ship Bottom Ordinance 2025-09C status per Borough of Ship Bottom municipal records. Beach Haven rental property regulations per Borough of Beach Haven Municipal Code, Chapter 159 (Rental Property). National vacation rental management commission averages (23-28%) per Rented.com industry data. Specific weekly rate ranges represent active 2026 listings and will vary by property condition, position, and timing. Net cap rate calculations are illustrative estimates for an investor framework and will vary based on actual contract terms, property specifics, and seller residency status. This article is informational and does not constitute legal, tax, or financial advice; LBI rental investors should engage a New Jersey real estate attorney and a tax advisor for transaction-specific calculations.

Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.