Anthony Licciardello | May 21, 2026

Mansiquan, NJ

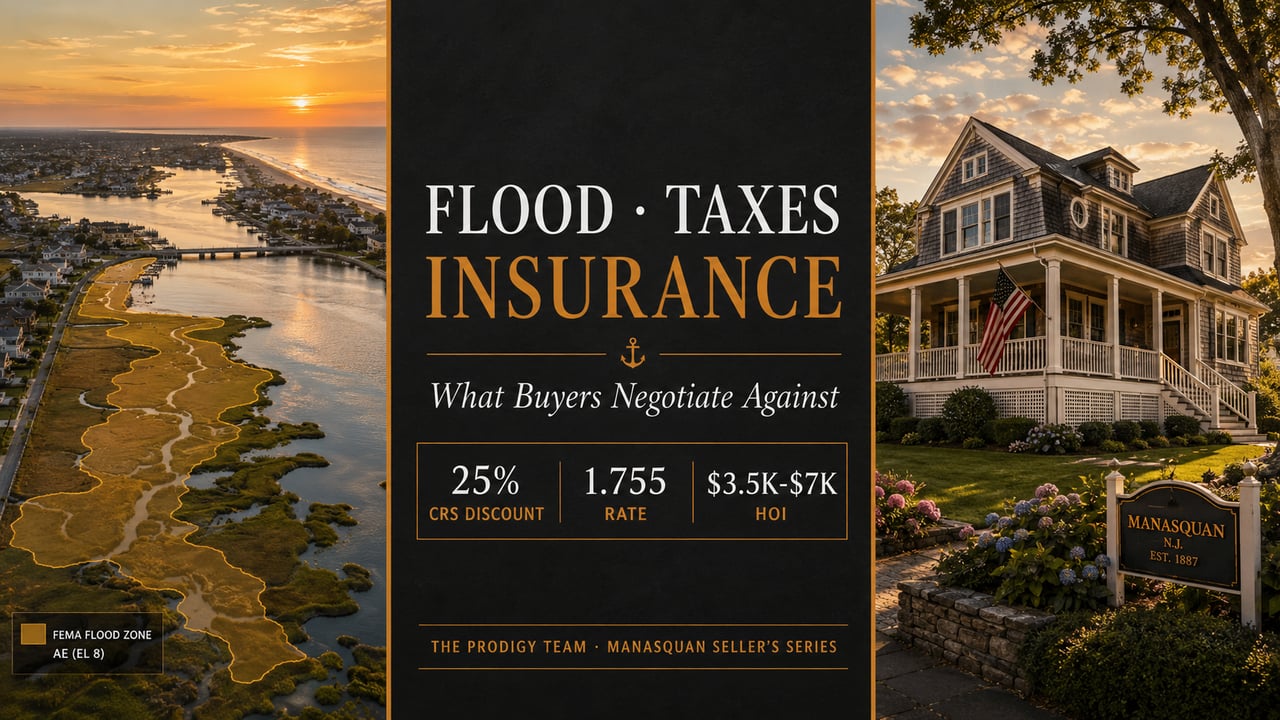

Every Manasquan buyer in 2026 walks into a showing with the same three concerns: flood insurance cost, property tax exposure, and homeowners insurance availability and pricing. These three line items together can add $15,000 to $30,000 per year to a buyer’s carrying costs — and on a $1.7M mortgage, that’s the difference between qualifying and being priced out. Smart buyers will use uncertainty around any of the three to push back on asking price. Smart sellers address all three before the negotiation starts. This is the final spoke in the Manasquan Seller’s Series, and it’s the one that determines whether your listing closes at full ask or gets chipped down 3-5% in the inspection-and-attorney-review window. For the full series context, start with our 2023–2026 Manasquan Seller’s Data Guide.

▸ The Three Pressure Points

Flood insurance under FEMA’s Risk Rating 2.0 (property-specific, not zone-based), property tax exposure including the contested 2026 Monmouth revaluation, and the increasingly expensive coastal homeowners insurance market. Buyers ask about all three. Sellers should answer before they’re asked.

Of the three pressure points, flood insurance is the one where Manasquan sellers have a genuine structural advantage — and most don’t know how to use it.

The Manasquan-specific facts. The borough participates in FEMA’s Community Rating System (CRS). As a direct result, every property in Manasquan automatically receives a 25% reduction on annual NFIP flood insurance premiums. The average Manasquan NFIP policy runs about $1,297 per year — well below what comparable V-zone shore homes in non-CRS communities pay. Roughly 1,493 active NFIP policies cover Manasquan properties.

Why Risk Rating 2.0 matters. Since April 2022, FEMA’s Risk Rating 2.0 has calculated premiums based on individual property characteristics — distance from water, structure foundation type, height of lowest floor relative to base flood elevation, prior claims, and replacement cost — rather than the old flood-zone classifications. This change means two Manasquan homes on the same block can carry very different premiums based on elevation, build quality, and flood vent compliance.

The seller’s opportunity. Most listing copy doesn’t mention the 25% CRS discount. Most listing agents don’t provide the property’s actual NFIP premium quote in advance. Buyers assume the worst — they price in the highest-tier flood premium from competing markets and discount the offer accordingly. The seller who provides the actual quote upfront removes that line item from the negotiation entirely.

▸ Seller Takeaway

Pull your property’s actual NFIP premium quote before listing. Include it in the listing materials. Foreground the 25% CRS discount in the copy. You eliminate one of the three negotiation pressure points before the buyer even tours.

▸ Broker’s Note

“Every Manasquan listing should include the actual flood quote in the disclosure package. It’s a 30-minute task that prevents a 3 percent price chip three weeks into attorney review.”

— Anthony Licciardello, Broker, The Prodigy Team

Property taxes in Manasquan are the line item buyers screen first — and the 2026 environment makes it the most consequential of the three pressure points. Two layers to address.

Layer one: the current numbers. Manasquan’s 2025 property tax rates run 1.755 general and 0.978 effective. On a $1.7M assessed-value home, that translates to roughly $16,000 to $17,000 per year in current property taxes. For a buyer underwriting carrying costs at the average single-family price point, that’s 11% of the purchase price spread annually — meaningful, but in line with Monmouth County peer averages.

Layer two: the revaluation litigation. Manasquan is one of five Monmouth County municipalities — alongside Allentown, Belmar, Marlboro, and Wall — that have formally contested the state-approved order requiring a districtwide revaluation for the 2026 tax year, with annual reassessments to follow in 2027. The litigation is documented on page five of the Monmouth County 2025 Annual Reassessment Summary. The outcome is genuinely uncertain.

What buyers actually fear. If the revaluation proceeds, the borough’s tax burden gets redistributed based on current market values rather than legacy assessments. Properties that have appreciated most since the last reassessment face the heaviest delta. For homes purchased pre-2022 in the Beach Block or North End zones, that potential upward swing is the single largest unknown in the carrying-cost equation. A buyer running a 30-year ownership model sees the difference between a stable annual tax bill and a stepped-up one as a six-figure swing over the hold period.

| Tax Scenario | $1.7M Home Annual | Notes |

|---|---|---|

| Current rate, current assessment | ~$16,600 | 1.755 general × current assessment |

| Revaluation succeeds (worst case) | $20K–$25K | Reassessed at full market value |

| Litigation succeeds (likely) | ~$16,600 | Status quo maintained |

| Compromise outcome | $18K–$20K | Phased reassessment |

The smart seller doesn’t dismiss the buyer’s concern. They surface the issue directly, explain the litigation status, and present a defensible range. A buyer who hears “we’re contesting it and even if it proceeds, here’s the range” goes back to their underwriting with a usable number. A buyer who hears nothing assumes the worst-case scenario.

▸ The Revaluation Read

“The revaluation question is going to come up in every Manasquan negotiation in 2026. Sellers who answer it first control the narrative. Sellers who wait for the buyer to raise it concede the price.”

— Anthony Licciardello, Broker, The Prodigy Team

▸ Seller Takeaway

Provide a one-page tax summary with the listing: current rate, current assessment, current annual bill, plus a brief paragraph on the revaluation litigation and the realistic outcome range. Surface the issue before the buyer’s attorney does.

The third pressure point is the one fewest sellers address — and the one becoming most expensive year over year. Homeowners insurance for coastal New Jersey homes has been getting harder to obtain and more expensive to maintain for five consecutive years.

The market dynamics. Several national carriers have either exited coastal New Jersey entirely or substantially restricted new policy underwriting. The carriers still writing coastal policies have raised premiums materially — coastal homeowners insurance for a typical Manasquan single-family home in 2026 runs $3,500 to $7,000+ per year depending on replacement cost, distance from water, and roof age. Premium high-value homes ($2M+) can push north of $10,000 annually.

What changes for the seller. A buyer who can’t obtain homeowners coverage cannot close on a mortgaged property. A buyer who obtains coverage at the high end of the range may walk if the premium materially impacts their debt-to-income calculations. This isn’t a price-chip risk — it’s a deal-breaker risk.

The seller’s defensive move. Engage a local insurance broker before listing. Get an indicative quote on what the next buyer would pay for replacement-cost coverage. If the quote comes in reasonably (under $5,000 for a sub-$2M home, under $8,000 for premium-tier), include it in the listing materials. If the quote comes in high or carriers are reluctant to write coverage, that’s information the seller needs to know before negotiating — either to address roof/electrical/plumbing issues that drive premiums, or to price the listing realistically.

▸ Seller Takeaway

Run the homeowners insurance quote before listing, not after the buyer’s offer is on the table. If the quote is favorable, market it. If it’s unfavorable, address the underlying issues (roof, electrical, plumbing) before the listing goes live.

Every Manasquan buyer’s mortgage application requires the lender to verify total housing costs — principal, interest, taxes, and insurance (PITI), plus HOA fees where applicable. The three pressure points above all flow into the “TI” portion. Here’s what a realistic 2026 Manasquan single-family carrying-cost stack looks like:

| Line Item | Annual | Monthly |

|---|---|---|

| Mortgage (P&I) | $98,000 | $8,167 |

| Property tax | $16,600 | $1,383 |

| Homeowners insurance | $5,000 | $417 |

| Flood insurance (NFIP) | $1,300 | $108 |

| Total PITI + Flood | ~$120,900 | ~$10,075 |

Assumes $1.7M purchase, 20% down ($1.36M mortgage), 6.1% 30-year fixed rate, current Manasquan tax rate, mid-range coastal insurance, average NFIP premium with CRS discount.

A buyer running this math sees roughly $10,000 per month in PITI plus flood. The three pressure points in this post represent the “TI” and flood pieces — collectively $1,908 per month, or 19% of total carrying cost. Any uncertainty in any of those three line items materially shifts the underwriting outcome. Sellers who lock those numbers down with documentation create certainty in the buyer’s mortgage application process.

▸ Broker’s Note

“A pre-prepared carrying-cost worksheet in the listing package is the single most underused seller tool I see. Two thousand dollars in ‘TI’ uncertainty kills more deals than $20,000 in pricing disagreement.”

— Anthony Licciardello, Broker, The Prodigy Team

The defensive strategy for the three pressure points is the same: surface the information upfront in a disclosure package, before the buyer’s attorney or underwriter raises it. The package should include:

▸ Seller Takeaway

The disclosure package costs roughly 4-6 hours of broker and attorney time to assemble. It typically saves 2-5 percentage points in negotiation. The ROI is the highest of any single seller-side investment in the listing process.

Even with the best disclosure package, buyers will probe. Three common pushback patterns and the seller’s effective response:

Pushback one: “The taxes are going to spike with the revaluation.” Response: present the four-scenario table from Section 02. Show the buyer the realistic range, not the worst case. Explain that the litigation status remains active and the most likely outcome based on similar five-municipality coalitions is a partial settlement or phased reassessment, not a wholesale spike. Offer to include a price adjustment in attorney review contingent on the revaluation outcome by a specific date — rarely needed but a credibility move.

Pushback two: “Homeowners insurance quotes I’m getting are way higher than yours.” Response: this is genuine market variability under Risk Rating 2.0 and carrier underwriting. Provide the buyer with the broker contact who ran the seller’s quote. Often the buyer’s own broker is overpricing because they don’t know the property-specific mitigation features (newer roof, flood vents, generator, etc.). A second quote from the seller’s broker often closes the gap.

Pushback three: “Total carrying costs are higher than I budgeted.” Response: this is sometimes a real qualification issue and sometimes a negotiation tactic. Distinguish between them by asking whether the buyer’s lender has issued a conditional approval. If yes, the carrying cost concern is negotiation theater. If no, the buyer may genuinely need a lower purchase price to qualify. The seller’s decision depends on whether they want this deal or the next one.

▸ Seller Takeaway

Every pushback on flood, taxes, or insurance is a buyer signaling either real concern or negotiation testing. The pre-prepared disclosure package neutralizes both. When the seller has answered the question first, the buyer’s leverage on it drops to zero.

Over six posts, this series has covered the full Manasquan seller’s decision tree: the four-year MOMLS data context, the five-zone submarket pricing framework, the eight-week spring listing window, the three-town peer comparison against Spring Lake and Sea Girt, the teardown sale to the builder buyer market, and now the three pressure points buyers will use to negotiate against asking price.

The thread connecting all six posts: data wins. The Manasquan seller who knows the borough-level appreciation arc, the zone-specific pricing range, the seasonal window, the cross-town comp set, the builder pro forma math, and the buyer’s actual carrying-cost stack is the seller who closes at full ask. The seller who works from generic shore-real-estate intuition is the seller who concedes 3-5% in the inspection-and-attorney-review window. The 2026 shore real estate environment rewards preparation over instinct.

▸ The Bottom Line

Flood insurance, property taxes, and homeowners insurance together represent 19% of a Manasquan buyer’s monthly carrying cost. Each of the three is a potential negotiation pressure point. A pre-listing disclosure package — NFIP quote, tax statement plus revaluation note, indicative homeowners insurance quote, and a populated carrying-cost worksheet — neutralizes all three. The package costs 4-6 hours to assemble and typically saves 2-5% in negotiation. That’s $34,000 to $85,000 on a $1.7M listing. The math is unambiguous.

Yes. The borough participates in FEMA’s Community Rating System, and every Manasquan property automatically receives a 25% reduction on annual NFIP flood insurance premiums. The average Manasquan NFIP policy runs about $1,297 per year, with roughly 1,493 active policies borough-wide.

The litigation is active. Manasquan is one of five Monmouth municipalities contesting the state-approved order, along with Allentown, Belmar, Marlboro, and Wall. Outcomes range from full litigation success (status quo maintained) to partial settlement (phased reassessment) to full revaluation. Most realistic outcome is a compromise that produces modest tax adjustments rather than a wholesale spike.

For a sub-$2M single-family home with current systems and a roof under 15 years old, $3,500 to $7,000 per year is the realistic range. Premium-tier homes ($2M+ replacement cost) push north of $10,000 annually. Older roofs, knob-and-tube electrical, and original plumbing all push premiums up materially.

Implemented in 2022, Risk Rating 2.0 prices NFIP policies based on individual property characteristics — distance from water, structure foundation, elevation, prior claims, and replacement cost — rather than the old flood-zone-based system. For Manasquan, this means two homes on the same block can carry very different premiums based on property-specific features. The 25% CRS discount applies on top of the Risk Rating 2.0 calculation.

Current NFIP flood insurance quote with the 25% CRS discount line item, FEMA flood zone map excerpt annotated to the property, current property tax statement with rate breakdown, a one-paragraph revaluation status note, indicative homeowners insurance quote from a local broker, a carrying-cost worksheet showing PITI plus flood, and proactive disclosure of any prior flood or water events. Together, the package costs 4-6 hours to assemble and typically prevents 2-5% in negotiation chips.

▸ The Final Step

The flood quote, the tax summary, the homeowners insurance quote, and the carrying-cost worksheet take 4-6 hours of professional time to assemble. They save 2-5% in negotiation. On a $1.7M Manasquan listing, that’s a six-figure return on a half-day’s preparation.

Request Your AuditOr call direct: (718) 873-7345

▸ The Complete Manasquan Seller’s Series

Pillar · The 2023–2026 Seller’s Data Guide · Spoke 1 · Pricing Your Manasquan Home by Submarket · Spoke 2 · When to List: Seasonality and the Spring Premium · Spoke 3 · Manasquan vs. Spring Lake vs. Sea Girt · Spoke 4 · Selling a Tear-Down to the Builder Buyer Market · Spoke 5 · Flood, Taxes, Insurance: What Buyers Will Negotiate Against in 2026

Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.