Anthony Licciardello | May 27, 2026

Long Beach Island, NJ

FEMA stopped requiring them. Most LBI owners stopped getting them. And then the smart ones started getting them again — because the math changed twice, not once.

Under Risk Rating 2.0, the NFIP no longer requires an Elevation Certificate (EC) for most policies — FEMA pulls its own elevation data from federal LiDAR and satellite mapping databases. That's the change everyone heard about. The change most LBI owners missed: FEMA's automated data is sometimes wrong, sometimes significantly. When the automated data underestimates your home's actual elevation, you're paying a premium for a freeboard credit you should already be receiving. A $400–$700 EC from a licensed surveyor can produce four-figure annual savings if it shows your home is higher than FEMA's automated read assumed. ECs also remain functionally required by most private flood carriers, by lenders doing LOMA filings, and by careful buyers doing pre-offer due diligence.

For thirty years, the Elevation Certificate was the most important piece of paper in any LBI flood insurance file. It told the NFIP what the home actually was — how high the first floor sat, how the foundation was built, what the lowest mechanical equipment elevations were — in a format the rating system could read. Without an EC, an owner in a Special Flood Hazard Area paid the highest rate the program would charge them. With an EC, they paid for the home they actually had.

That dynamic changed when Risk Rating 2.0 rolled out. FEMA built its own elevation pipeline using federal LiDAR data, removed the mandatory EC requirement, and told owners they no longer needed to send a surveyor to the property to get rated correctly. For most policies, that's true at face value. But "rated correctly" is doing a lot of work in that sentence, and the smart owners — the ones who actually compared FEMA's automated read against their home's real elevation — discovered that the automated read was often conservatively wrong. This article explains where the EC still matters, why it can still pay for itself in a single renewal cycle, and how to use it strategically as a buyer or seller in the post-Risk Rating 2.0 environment.

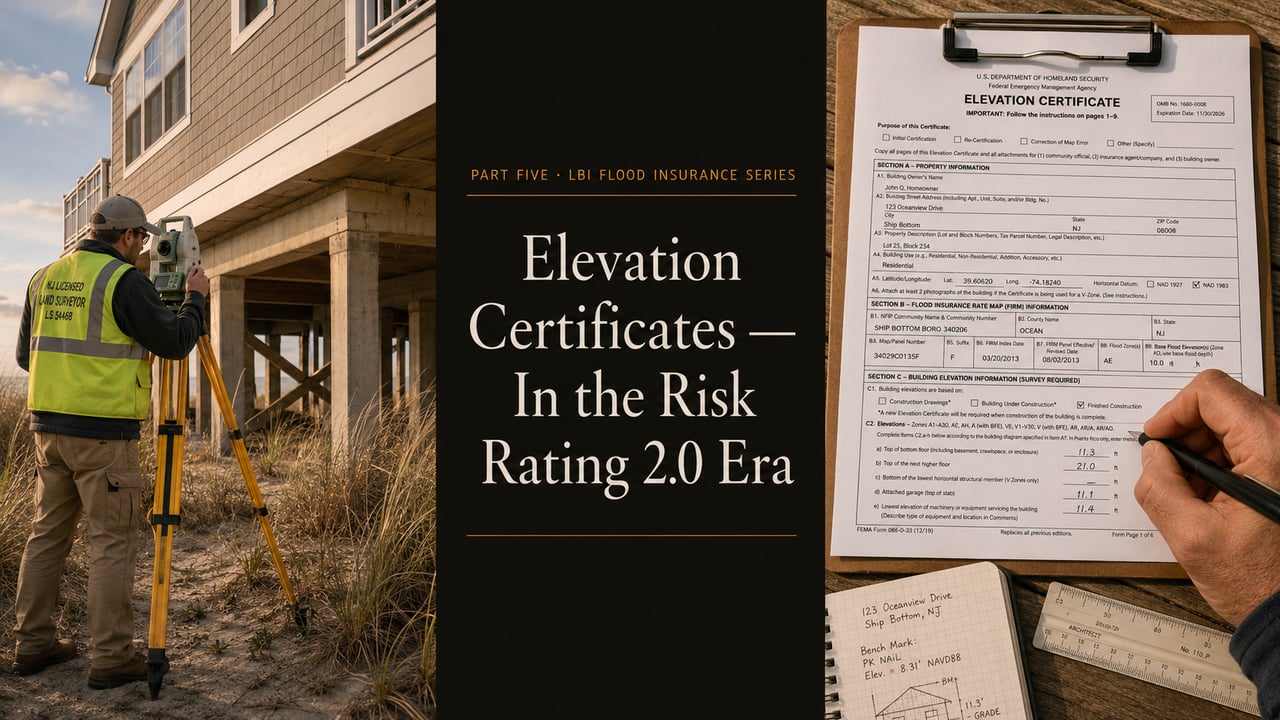

An Elevation Certificate is FEMA Form 086-0-33 — a standardized document that records the physical elevations of a structure relative to the surrounding ground and relative to Base Flood Elevation (BFE). It must be completed by a licensed land surveyor, professional engineer, or registered architect, and the signatory takes professional liability for the measurements recorded on it.

The document captures, at minimum, the following elevations for a residential structure: the lowest floor (including any basement or subgrade space), the next-highest floor, the lowest adjacent grade beside the structure, the highest adjacent grade, the elevation of any attached deck or stairs, and the elevation of any machinery or equipment servicing the building. It also documents the construction characteristics — foundation type, presence of flood vents, basement status — that influence how the structure is rated.

Every measurement is referenced to a specific vertical datum — typically the North American Vertical Datum of 1988 (NAVD 88) on current LBI surveys, replacing the older National Geodetic Vertical Datum of 1929 (NGVD 29) that appears on legacy ECs. Old ECs on the NGVD 29 datum can still be used for insurance purposes, but the datum conversion needs to be done correctly or the resulting elevations will be off by approximately one foot — enough to matter in a Risk Rating 2.0 worksheet.

The official document and full instructions are published at FEMA's Elevation Certificate page, along with the form itself in fillable PDF format.

When FEMA launched Risk Rating 2.0 in October 2021, the agency simultaneously eliminated the mandatory EC requirement for most NFIP policies. The reasoning was logistical and technological: federal LiDAR coverage of coastal communities had matured to the point where FEMA could pull elevation data from its own datasets without requiring owners to commission individual surveys. The shift was framed as a customer-friendly simplification — one less hoop to jump through during policy binding.

The reality was more nuanced. FEMA's automated elevation pipeline does provide a reasonable read for the majority of homes — and for the homes where it reads accurately, the program now works exactly as designed: bind a policy, get rated against the automated data, pay the resulting premium. No surveyor required.

But automated elevation data has limitations. LiDAR captures ground surface elevation, not the elevation of the lowest finished floor of a specific structure — the value FEMA infers structurally. For homes built well above grade on tall pilings, that inference can underestimate true first-floor height by a foot or more. For homes with unusual foundation geometries, additions built at different elevations, or recent modifications not yet reflected in the automated data, the underestimate can be larger. And in every case where the automated data underestimates your home's true elevation, you are paying a premium for freeboard credit you should already be getting.

FEMA's response to this gap is straightforward: owners who believe the automated data is wrong can voluntarily submit an Elevation Certificate showing the true elevation, and FEMA will rate the policy against the EC data instead. The EC is no longer mandatory, but it remains the operative document for correcting the rating when correction is warranted.

"Optional" under NFIP rules is not the same as "irrelevant." There are six specific scenarios where a current Elevation Certificate remains either functionally required or strongly recommended for an LBI property:

1. You suspect FEMA's automated data is wrong. If your home is elevated well above grade and your premium feels disproportionate to the home's actual freeboard, the most common explanation is that FEMA's automated read is underestimating your first-floor height. A licensed surveyor's EC is the corrective instrument.

2. You're filing a Letter of Map Amendment (LOMA). Challenging your flood zone designation requires an EC showing the natural ground elevation is at or above BFE. Covered in detail in Part Three of this series; the EC is the documentary backbone of the filing.

3. You're shopping private flood carriers. Most private flood carriers still require a current EC as part of their underwriting process. They are putting their own capital on the line and want documented proof of the structural profile, not FEMA's automated inference. If you're cross-shopping NFIP against private — and as Part Six of this series will cover, you should be — having an EC on file is functionally a prerequisite for getting competitive private quotes.

4. You've completed substantial mitigation work. If you've elevated the structure, added engineered flood vents, raised your mechanical equipment, or otherwise improved the home's "How" pillar profile, a post-improvement EC documents the new condition for your carrier. Without it, the rating worksheet may not credit the improvement.

5. You're selling and want to protect deal certainty. A current EC in the listing materials neutralizes the most common source of buyer panic about LBI premiums — the unknown. We'll cover the seller-side EC strategy in detail in Chapter Seven.

6. You're buying and want a real number before closing. Pre-offer or pre-closing ECs let a buyer pull a binding insurance quote against documented elevation data, not the seller's representations or FEMA's automated inference. For any LBI purchase above the typical price point, this is increasingly standard buyer-side due diligence.

A completed Elevation Certificate is structured in eight sections. Knowing what each section captures helps you read the document quickly when you receive one — and helps you identify the lines that matter most for premium math.

Section A — Property Information. Building owner, address, lot and block, latitude/longitude coordinates, building use, and a designation of whether the building is residential or non-residential.

Section B — Flood Insurance Rate Map Information. The FIRM panel number, effective date, flood zone designation, Base Flood Elevation, and whether the building is in a Coastal Barrier Resources System area. This is where the V-Zone, AE, or Coastal A designation from Part Three of this series is recorded.

Section C — Building Elevation Information. The core of the document for insurance purposes. Records the lowest floor elevation, the next-highest floor, the elevation of attached structures, the elevations of machinery and equipment, the lowest adjacent grade, and the highest adjacent grade. These are the numbers Risk Rating 2.0 cares about most.

Section D — Surveyor, Engineer, or Architect Certification. The signatory's professional license number, name, address, and signature certifying the measurements. This is what gives the document its evidentiary weight.

Section E — Building Measurements for Zone AO and Zone A. Used only for properties in shallow-flooding A or AO zones without specified BFE. Rarely applicable on LBI.

Section F — Property Owner Certification. Used when the building owner is self-certifying certain measurements rather than having a surveyor do it. Carries less evidentiary weight than Section D and is generally not used for premium-rating ECs.

Section G — Community Information. Local floodplain administrator's certification used for permit and floodproofing documentation. Required for certain code-related uses but not for routine insurance rating.

Section H — Building Photographs. Attached photographs of all sides of the structure, plus close-ups of any flood vents and the foundation. These visually corroborate the structural information recorded in Section C.

On LBI, a residential Elevation Certificate from a licensed land surveyor typically costs between $400 and $700. Premium pricing applies for properties with complex foundation geometries, recent modifications requiring detailed field measurement, or properties requiring expedited turnaround during peak transaction season.

The timeline. Scheduling lead time for LBI surveyors varies seasonally — summer transaction volume can push scheduling out 4 to 6 weeks, while off-season turnaround can be as fast as 2 weeks. The on-site fieldwork itself is usually completed in a single 1- to 2-hour visit. The bulk of the post-visit time is data processing, datum reconciliation, photograph annotation, and final certification — typically 1 to 2 weeks from fieldwork to delivered EC.

What you should provide. Surveyors work most efficiently when they have access to existing documentation — prior ECs (even outdated ones), construction drawings, foundation as-built diagrams, and any permits related to elevation or substantial improvement work. If the home has been recently modified, having the contractor's documentation available speeds the fieldwork.

The ROI math. An EC pays for itself when it documents elevation that produces a premium reduction larger than its cost. For an LBI home where FEMA's automated data is meaningfully underestimating true first-floor height, even a single year of corrected premium typically covers the $400–$700 fee. For homes where the EC merely confirms FEMA's automated data was correct, the investment is sunk — though it still provides documentation value for resale, mitigation crediting, and private carrier shopping. The expected-value math favors the EC for any LBI property with non-trivial freeboard above BFE.

Elevation Certificates technically have no expiration date. The measurements recorded on the document remain valid as long as the underlying physical conditions remain unchanged. That language is important — the EC is current as long as the home is current. Anything that changes the structure or its elevation profile can invalidate the existing EC.

Triggers that require a new EC: elevating the home, modifying the foundation, adding or removing flood vents, finishing or unfinishing a lower enclosure, building an addition that changes the lowest floor, raising or lowering mechanical equipment, regrading the lot, or any other physical change that affects the values recorded in Section C.

Triggers that do not require a new EC: interior renovation that doesn't affect the lowest floor or foundation, cosmetic exterior updates, landscaping that doesn't change adjacent grade, replacing mechanical equipment in the same location, and changes of ownership (the EC follows the home, not the owner).

The FIRM revision wrinkle. Even an EC that's structurally still accurate may need updating if FEMA revises the Flood Insurance Rate Map covering the property. New FIRMs can change the Base Flood Elevation referenced in Section B, the flood zone designation, or both. The structural measurements in Section C remain valid, but the comparison values in Section B may no longer reflect the current map. In practice, a Section B update typically requires a fresh signature and certification — meaning a new EC, even if the structural data hasn't changed.

Practical recommendation. If your most recent EC predates the most recent FIRM revision affecting your property, or predates any meaningful structural work on the home, get a current one. The cost is modest, the process is standardized, and the resulting document is the operative reference for every premium conversation, lender requirement, and resale disclosure for the foreseeable future.

Sellers. A current EC in the listing materials is one of the highest-ROI seller-side disclosures available on LBI. It accomplishes three things simultaneously: it neutralizes buyer panic about unknown flood premiums, it gives the buyer documentation to pull a binding insurance quote against actual elevation data, and it signals to the buyer's broker that the seller has done their homework. For LBI properties priced above the typical median, a $500 EC paid for at listing has materially better deal-protection value than a $500 staging upgrade.

The discipline is to commission the EC before the listing photos, not in response to a buyer's request. Once a buyer asks for the EC during due diligence, the document becomes a contingency item; once it's already in the marketing package, it becomes a confidence signal. Same document, different transactional weight.

Buyers. If the listing does not include a current EC, the right move is to either request that the seller commission one during attorney review or commission one yourself as part of pre-contract due diligence. The $400–$700 cost is small relative to the deal economics, and the information meaningfully de-risks the most volatile line item in the all-in carrying cost.

For buyers cross-shopping LBI against other shore submarkets, the EC strategy travels — the same logic we walk through in our Manasquan flood, taxes, and insurance breakdown applies on any barrier-island or shore-front purchase. The exposure profile shifts; the underwriting discipline doesn't.

The post-closing EC. If you closed on an LBI home without an EC in the file and you're now paying NFIP premiums you suspect are over-rated, the post-closing EC is the corrective instrument. Order it, submit it to your carrier, and request a rating worksheet update at renewal. Even if the resulting premium reduction is modest, the documentation creates the paper trail you'll want for resale and for any future private-carrier shopping.

For every LBI listing The Prodigy Team takes, the first conversation with the seller covers EC status. If a current EC exists, we incorporate it into the listing materials and use it to anchor the carrying-cost narrative in the property's marketing copy. If a current EC does not exist, we commission one before the property goes to market — paid for as a listing expense, recouped through faster days-on-market and cleaner negotiation dynamics.

For every LBI purchase we represent, the EC review is part of the pre-offer workflow. We confirm whether a current EC exists, read the structural data against the property's listing representations, and identify any discrepancies that need to be resolved before the offer is structured. For properties without an EC available, the offer typically includes a contingency requiring delivery of a current EC during attorney review.

If you're considering an LBI purchase or sale and want a clear read on the EC status, the elevation data, and the resulting premium and rating implications before any commitment, that's part of the underwriting we run on every transaction.

Three reasons. First, FEMA's automated elevation data is sometimes wrong, and an EC corrects the rating when it underestimates true first-floor height. Second, most private flood carriers still require an EC as part of their underwriting, so cross-shopping requires the document. Third, the EC remains required for Letter of Map Amendment filings, post-mitigation rating updates, and pre-sale documentation. Optional under NFIP rules is not the same as functionally unnecessary.

No. Elevation Certificates must be completed and signed by a licensed land surveyor, professional engineer, or registered architect — a credentialed signatory who takes professional liability for the measurements recorded on the document. Real estate agents, insurance brokers, and home inspectors cannot complete or sign an EC. Always work with a properly licensed signatory.

Technically, ECs do not expire — the document remains valid as long as the underlying physical conditions are unchanged. In practice, an EC older than 10 years should be reviewed carefully against any subsequent FIRM revisions, datum changes, or structural modifications to the home. ECs on the older NGVD 29 datum require correct conversion to the current NAVD 88 datum to remain rateable. When in doubt, commission a current EC rather than rely on a legacy document of uncertain currency.

Not always. An EC can lower your premium when it documents elevation higher than FEMA's automated data assumed, when it documents structural improvements that the rating worksheet hasn't yet credited, or when it supports a successful Letter of Map Amendment. It can also confirm that FEMA's automated read was already accurate, in which case the EC produces no premium change. The investment is best understood as buying information — and on most LBI homes with meaningful freeboard, the information is favorable.

In New Jersey, there is no statutory requirement for the seller to provide an Elevation Certificate at closing. The standard NJ Property Condition Disclosure Statement covers known material defects but does not require EC delivery. However, New Jersey's Flood Risk Disclosure Law (effective 2024) does require sellers to disclose known flood risks and prior flood damage in writing, and many LBI buyers — particularly those purchasing above typical price points — make EC delivery a contractual contingency during attorney review. Practically, providing an EC is a buyer-confidence signal; legally, it is not currently mandated.

Anthony Licciardello is the founding broker of The Prodigy Team, an independent brokerage serving Staten Island and the New Jersey shore. He works with buyers and sellers across Long Beach Island, Monmouth County, Ocean County, and Union County markets.

Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.