Anthony Licciardello | May 17, 2026

Ocean County, NJ

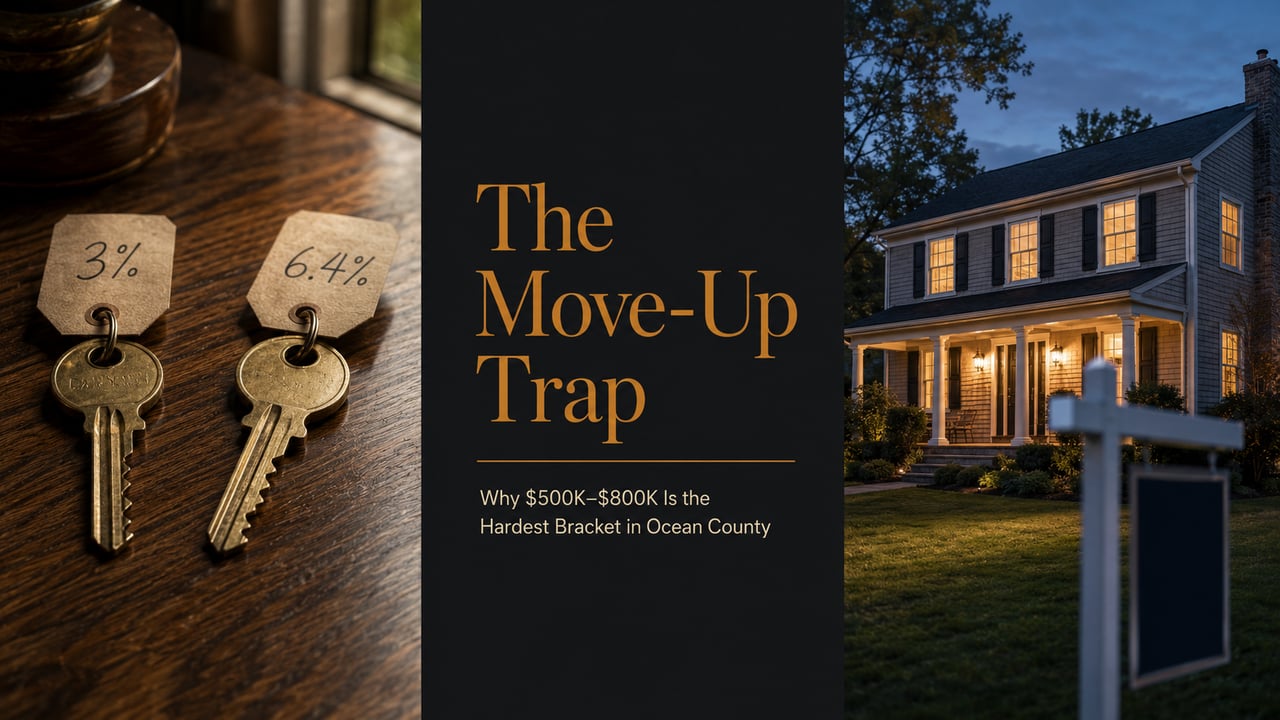

In Post 3, we mapped how the Spring 2026 correction is unfolding differently across each Ocean County submarket. This post moves from where the correction is happening to why it's happening — and specifically why one price band is bearing the brunt of it. Across Brick, Toms River, Stafford, Lacey, and Barnegat, the $500,000-to-$800,000 move-up tier is the single most contested bracket in Ocean County real estate this spring. Buyer hesitation in this range isn't an attitude problem. It's mortgage arithmetic.

Every Ocean County seller listing a home priced between $500K and $800K is competing for a buyer pool that, for the first time in fifteen years, has to do a kind of math their parents never had to do — and one that the post-2008 generation of homebuyers never faced either. Understanding that math is the difference between pricing a move-up home that sells in 30 days and one that sits for 90.

Across Ocean County, the largest single price bracket by transaction volume is the $500K–$800K range. This is the natural landing spot for two distinct buyer profiles: families upgrading from a starter home in the $350K–$450K range, and households relocating into Ocean County from the more expensive Monmouth, northern New Jersey, or New York metropolitan area submarkets. Brick, Stafford, Lacey, and the upper end of Toms River all do their highest-volume business in this exact bracket.

When this bracket gets harder to transact in, the entire local market slows. Starter-home sellers can't move up. Out-of-area transplants can't enter. Inventory builds, days-on-market extends, and the correction described in Post 2 deepens. The Spring 2026 dynamic in Ocean County is, more than anything else, a story about what's happening — or not happening — to the move-up buyer.

And the move-up buyer in 2026 is, almost without exception, sitting on a mortgage rate they refuse to give up easily.

Per Redfin's analysis of Federal Housing Finance Agency data, 52.5% of mortgaged American homeowners currently hold a mortgage rate below 4%. Roughly one in five — 20.4% — hold a rate below 3%. These are the rates that were available during the 2020-2022 refinance boom, when Freddie Mac's average 30-year fixed mortgage rate dropped as low as 2.87% in August 2021 and stayed in the 3.0%-3.2% band through the end of that year.

Five years later, those homeowners face a specific and uncomfortable decision. Freddie Mac's most recent Primary Mortgage Market Survey reading places the 30-year fixed mortgage rate at 6.36% as of May 14, 2026 — virtually unchanged from the prior week, and within the 6.30%-6.40% band that has held through most of the spring. That's not a small rate change for someone considering trading homes. It's roughly 3.4 times the rate at which they originally locked in.

This is the structural reality every Ocean County move-up tier seller faces in Spring 2026. It's not that buyers don't want your home. It's that the math of giving up a 3% mortgage to take on a 6.36% mortgage on a more expensive house is, for many otherwise interested households, prohibitive — and they know it before they ever walk through your front door.

Consider a representative Ocean County household. They bought a starter home in 2021 for $400,000, putting 20% down and financing $320,000 at the prevailing 3.0% rate. Today their family has grown, and they're looking at a $650,000 move-up home in Brick, Stafford, or Lacey. Same 20% down, $520,000 financed at today's 6.36% rate. Here's what changes on their monthly statement:

This is the financial reality your buyer pool is sitting with when they evaluate your $650,000 move-up listing in Toms River or Stafford. They are not deciding whether your home is worth $650,000. They are deciding whether an additional $1,890 a month — for the next 30 years — is worth the upgrade. That decision-making framework explains nearly everything about Spring 2026 buyer behavior in the move-up tier.

Move-up buyers in 2021 were not doing this math. They were doing a different math: how much home can we afford if our family grows. They focused on bedrooms, square footage, school district. The financing was a footnote — at 3% rates, even doubling the loan principal added only a few hundred dollars to the monthly payment. The shape of the home mattered more than the cost of capital.

In 2026, the math has inverted. Buyers walk into your Ocean County open house with a mortgage calculator already open on their phone. They aren't asking, "Is this our forever home?" They're asking, "What does this house do to our monthly?" And every additional $25,000 in your asking price represents roughly $156 per month in additional payment they have to absorb for the next three decades. That changes how every showing, every offer, and every counter-negotiation feels.

The 2026 move-up buyer isn't comparing your home to their dream of a forever home. They're comparing it to their current home — the one with the 3% mortgage they're about to walk away from. That's a much harder comparison for any seller to win.

The practical implication for sellers: aspirational pricing on a $500K-$800K move-up home produces a more severe form of the rejection described in Post 2's capitulation timeline. Buyers don't just pass on the home — they pass on it with mathematical precision, having calculated to the dollar how much your asking price would cost them per month. The rejection is not emotional. It's arithmetic.

“Every move-up buyer I sit with in 2026 is doing the same calculation: how much per month does this cost me, and is that worth what I'm giving up. The sellers who understand that calculation price for it. The sellers who don't, sit.”

On a $560,000 loan — the typical 80% LTV financing for a $700,000 Ocean County move-up home — small rate movements translate into large monthly payment changes. Here's the sensitivity, calculated from current Freddie Mac PMMS data:

| If Rates Are | Monthly P&I | Annual P&I | vs. Today |

|---|---|---|---|

| 6.00% | $3,357 | $40,290 | ▼ $131/mo less |

| 6.36% (current) | $3,488 | $41,858 | baseline |

| 7.00% | $3,726 | $44,708 | ▲ $238/mo more |

Calculated on a $560,000 30-year fixed-rate loan, principal and interest only. Property tax, insurance, and HOA dues add to actual monthly cost. Source rate: Freddie Mac PMMS, May 14, 2026.

The implication that matters most for sellers: every weekly Freddie Mac rate move expands or contracts your buyer pool measurably. When rates ticked down toward 6.06% in mid-January 2026, mortgage applications surged. When they crept back above 6.40% in March, application volume softened. Your listing is exposed to that volatility in ways that simply did not exist when rates were stable in the 3% range from 2020-2022.

Pricing precision matters more in the $500K-$800K bracket than anywhere else in Ocean County, but pricing isn't the only lever. Four tactical adjustments produce measurable improvements in outcomes for sellers in this tier.

“A rate buydown on a $700,000 listing can be the single most persuasive concession a seller offers in 2026. Buyers feel a $700-a-month payment reduction every month for a year. They don't feel a price cut the same way — and the cost to the seller is often less.”

Post 5 turns to the Ocean County submarket where the 2026 buyer psychology is most distinct: the 55+ adult community segment. Why a Holiday City or Leisure Village seller faces an entirely different buyer pool — one that's predominantly cash, predominantly patient, and predominantly comparing your home to a dozen others within walking distance. HOA fees, comparison sets, and the specific positioning strategies that produce contracts in 30 days instead of 75.

Read the adult community analysis →Per Redfin's analysis of FHFA National Mortgage Database data through Q2 2025, 52.5% of mortgaged U.S. homeowners hold a rate below 4%, and 20.4% hold a rate below 3%. Approximately 80% of all outstanding mortgages carry a rate below 6% — the current prevailing rate. The lock-in effect is gradually easing as life events force selective moves, but it remains the dominant force constraining move-up tier inventory in 2026.

A 2-1 temporary rate buydown on a $560,000 loan typically costs $14,000-$16,000 paid upfront by the seller at closing. In exchange, the buyer's first-year interest rate drops by 2 percentage points (to roughly 4.36% on today's 6.36% rate), and the second-year rate drops by 1 point (to roughly 5.36%). The buyer's first-year monthly payment is approximately $700/month lower than the unbought-down equivalent. Specific costs vary by lender and the exact buydown structure; this is illustrative, not a guarantee for any individual transaction.

Two reasons. First, under-$500K buyers are disproportionately first-time buyers who don't have a 3% mortgage to give up — they're entering the market fresh, so the lock-in effect doesn't apply. Second, under-$500K affordability for median Ocean County income remains within reach even at 6.36% rates, while move-up tier affordability requires either dual high-income households or substantial equity transfer from a sold prior home. The math of the move-up trade is fundamentally different from the math of the first purchase.

There's no consensus forecast for rates dropping below 6% in the next 12-18 months — Fannie Mae, Realtor.com, and Zillow all currently project rates remaining in the mid-6% range through 2026 and into 2027. If you wait, you may also be waiting for inventory to expand (as more locked-in sellers reach the life-event tipping point), which could offset any rate-driven affordability improvement. The strategic answer depends on your specific timeline, equity position, and reason for moving — not on a market-wide rate prediction. A localized audit is the right starting point.

No — it concentrates most heavily in towns with significant inventory in the $500K-$800K range. Brick (~$520K median list), Stafford (~$650K), Lacey (~$550K), and the upper end of Toms River bear the brunt. The 55+ adult communities in Manchester and Berkeley experience a separate, parallel dynamic that we cover in detail in Post 5.

The framework we use at The Prodigy Team begins by identifying your specific target buyer pool and back-calculating the monthly payment that pool can absorb without breaking from their current housing cost by more than roughly $200/month. From there we work backward to a list price, then layer in submarket-specific DOM data and the Day-14 honeymoon-window requirement. The end result is typically a $10,000-$20,000 launch price window that the data supports — not a single point estimate. Sellers we've worked through this framework consistently net more on properly calibrated pricing.

A 30-minute pricing audit applies this entire framework — buyer payment math, monthly-affordability target, submarket DOM data, rate-buydown analysis — to your specific home. No obligation. No sales pitch. Just the math, and the strategic implications, clearly explained.

Request Your Audit →Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.