Anthony Licciardello | May 23, 2026

Summit, NJ

Why Distance to the Train Station No Longer Prices Your Summit Home the Way You Think

A geological ridge, a 2,800-space parking deficit, and a quiet 2016 policy decision have fractured Summit's pricing gradient into three distinct rings — and most sellers, and nearly every automated valuation model, are still pricing as if the old curve applied.

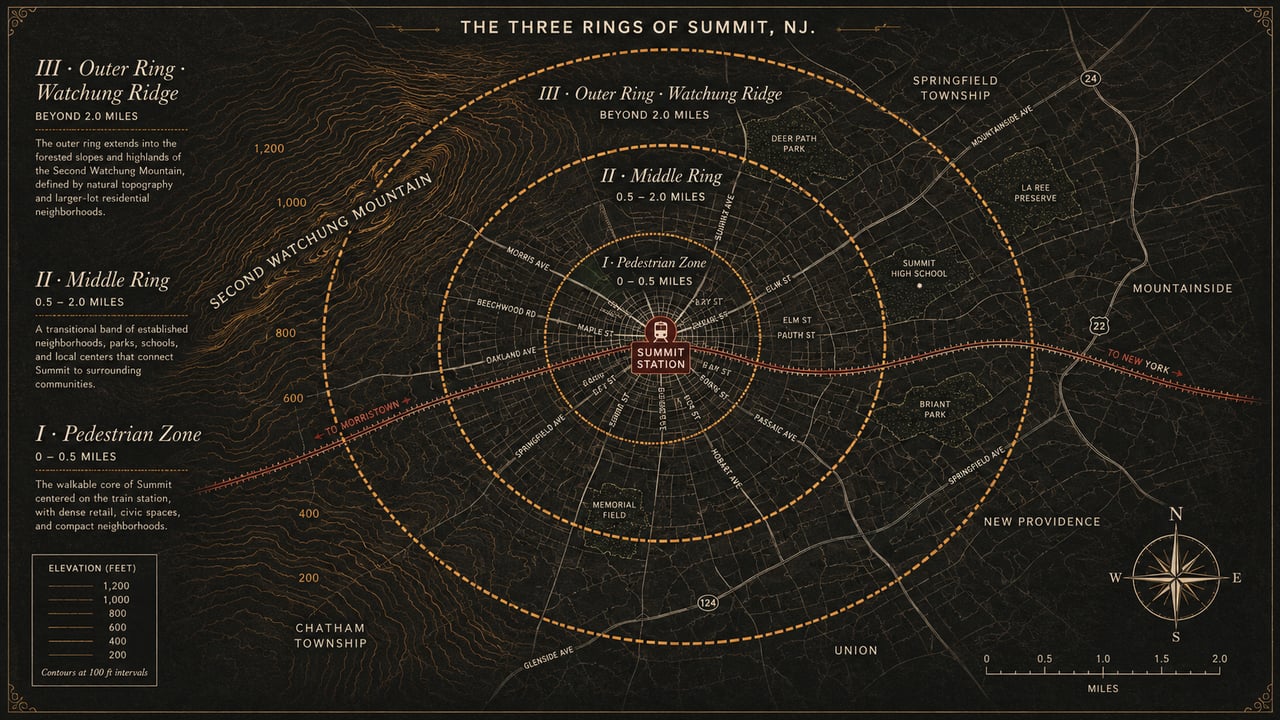

Summit's bid-rent curve is not a curve. It is a three-step function. The Pedestrian Zone (0–0.5 mi), the Middle Ring (0.5–2.0 mi), and the Outer Ring (>2.0 mi) are governed by different economics, respond to different buyer behavior, and capitalize different amenities. Sellers who price by Zillow's flat-plane logic systematically leave money on the table in two of the three rings — and overprice in the third.

In the standard economics of commuter suburbs, the formula is supposed to be elegant. A train station sits at the center of town. Property values radiate outward in a smooth, downward slope — what urban economists call the bid-rent curve. Walk faster to the platform, pay more. Drive farther, pay less. The math is so reliable that it is the assumption baked into Zillow's Zestimate, Redfin's estimate, and the automated valuation models running inside every bank's appraisal software. For most New Jersey commuter suburbs, this assumption is roughly correct.

Summit, New Jersey breaks the model. The break is not subtle, and it is not theoretical. It is the visible consequence of three structural forces: a Triassic basalt ridge whose elevation pulls high-end demand away from the train station, a chronic municipal parking deficit that historically taxed every property outside the walkable radius, and a 2016 rideshare policy intervention that quietly neutralized that tax without anyone calling it real estate news. Together these forces fracture Summit's pricing gradient into three discrete bands. Each band is governed by different buyer logic. Each is routinely mispriced by sellers who still treat their home as if a single, continuous curve applied to all of Summit's residential geography.

This six-part series is written for the Summit homeowner preparing to list in the next twelve months. It is not a market commentary, and it is not a recap of recent sales. It is a working pricing framework drawn from the spatial econometrics literature and adapted to the specific terrain, infrastructure, and policy environment of this town. We start, in this first installment, with the framework itself: the three rings of Summit, and the buyer logic that animates each.

The monocentric city model — the framework pioneered by William Alonso, Richard Muth, and Edwin Mills in mid-twentieth-century urban economics — holds that residential land values fall predictably with distance from a central node, almost always a transit hub or major employment center. The model has been validated across thousands of suburbs, in dozens of countries, for the better part of seventy years. In most commuter towns it remains roughly accurate. A single elegant downward slope, anchored at the station, decaying with distance.

The model begins to fail only when one of two conditions appears in the local geography. The first condition: a competing amenity — a coastline, a major park, an elevation ridge with viewshed — that creates a second, opposing source of value pulling demand away from the transit node. The second condition: constrained physical access to the transit node itself, such that the commuter who lives a mile away cannot reliably use the asset they are theoretically paying for.

Summit has both. The town sits on the eastern flank of the Second Watchung Mountain, a Triassic and Jurassic basalt ridge whose elevation runs from roughly 108 feet in the downtown valley basin to 581 feet on the upper crests of the Franklin Hill and ridge-line sections. The train station sits in the valley. The most prestigious viewsheds sit on the ridge. The two sources of value — transit access and topographical prestige — are inversely correlated by geography itself.

Then layer the parking constraint on top. The city operates approximately 2,800 commuter spaces across surface lots and structures. Historically those spaces saturated before 9:00 AM on a typical weekday. Residents pay a $10 annual permit, a $4 daily fee, and contend with a permit-and-lot system that does not guarantee a space on any given morning. Non-residents pay $14.95 daily at the Broad Street Garage with mandatory advance reservation. The Midtown Direct line is one of the most valuable commuter assets in northern New Jersey — but its economic value depends on whether you can actually reach the platform on a Tuesday at 7:43 AM.

These three forces — ridge, parking, and the 2016 rideshare program that partially neutralized the parking problem — do not produce a smooth gradient. They produce a three-step function. Sellers in downtown Summit and the immediate station radius live on one step. Sellers in the broad middle band of the town live on a second. Sellers on the upper ridge live on a third. The boundaries are sharper than they look on a topographic map.

Three forces broke the simple distance-and-train pricing logic in Summit: a basalt ridge, a parking deficit, and a quiet 2016 policy decision that most residents have never heard called real estate news. Together they fractured the bid-rent curve into three discrete steps.

The Pedestrian Zone is the band of residential geography from which a commuter can walk to the platform in under ten minutes, in any weather, without thinking about a car. Network distance — not Euclidean distance — matters here. A house that is 0.4 miles by sidewalk and 0.3 miles as the crow flies is a Pedestrian Zone house. A house that is 0.4 miles as the crow flies but requires walking around a ravine or down a no-sidewalk arterial is not.

This is the steepest portion of Summit's bid-rent curve. Inside this radius, the marginal value of an additional minute of walk-time is enormous and the parking constraint is irrelevant — you do not need a permit, you do not need to budget for a $4 daily fee, you do not need to monitor lot saturation by 8:30 AM. The asset you are paying for, the 30-minute express to Penn Station, is functionally a sidewalk extension of your front door. This is also the band where the downtown Summit retail corridor — the restaurants on Springfield Avenue, the coffee on Maple Street, the walking infrastructure — reinforces the commuter premium with a quality-of-life premium.

The annual prepaid parking rate Ring One residents do not pay. Add the $10 permit, the time cost of daily lot uncertainty, and the depreciation of a vehicle driven 0.7 miles each way, and the implicit annual access tax on Middle Ring commuters is materially higher than the headline parking fee suggests.

What capitalizes in Ring One: walking distance itself, lot size as a luxury indicator (because every square foot is on premium land), historic character on the older streets, and structural updates that signal turnkey readiness to the buyer who chose this band specifically to avoid car-dependence. What does not capitalize as heavily: garage capacity (less critical), additional square footage past a threshold (Pedestrian Zone buyers are often downsizing empty-nesters or young professional families who do not need the 5,800 sq ft house), and elevation (you are in the valley by definition).

The seller's mistake in this band is almost always one of two: pricing as if walkability is a soft amenity rather than the primary asset, or letting an outdated interior drag the listing's perceived value below what the location alone can carry. The buyer in Ring One has already self-selected for transit dependency. Lead the listing narrative there.

The Middle Ring is the part of Summit that the textbook monocentric model assumes is a smooth continuation of the Pedestrian Zone's downward slope. In Summit it has never been smooth. From roughly 0.5 miles to 2.0 miles out, residents are too far to walk daily but too close to write off the station entirely. They are park-and-ride commuters, and historically their access to the Midtown Direct line ran through a permit-and-lot system that frequently denied them the very thing their property value was implicitly priced on.

The empirical consequence is that, prior to 2016, the Middle Ring carried what urban economists call an infrastructure friction discount. A home in the Wyoming section at 1.3 miles from the station did not just sell for less than a comparable home at 0.4 miles — it sold for less than a clean linear extrapolation would have predicted. The slope of the value gradient in this band was artificially steepened by the unreliability of parking. The economic value of the train was discounted, parcel by parcel, by the daily uncertainty of whether you could actually use it.

Then, in the fourth quarter of 2016, the municipal government did something that no other suburban transit town in the United States had done at scale: rather than spending an estimated $5 million on additional parking infrastructure, Summit launched a subsidized rideshare partnership — first with Uber, later transitioned to Lyft — that gave residents a guaranteed, subsidized ride to and from the train station during commute hours. Initially the resident paid $2 per ride against the $4 daily parking fee. The program now sits at $4 per ride with a city-side cap, supported by an annual budget of approximately $120,000, entirely offset by non-resident parking revenue at the Broad Street Garage.

The seller's headline takeaway is this: the rideshare program functionally removed the spatial friction that had been suppressing Middle Ring values for decades. A residence in the Brayton School area or the broader 1.0-to-1.8-mile band is no longer constrained by whether the commuter can find a permit space at 8:15 AM. The Lyft pickup at 40 Railroad Avenue is the new last-mile infrastructure. And yet AVMs have not adjusted their pricing models to reflect this. Many listing agents have not either. The mispricing in this band, in both directions but predominantly to the downside, is the single largest hidden opportunity in current Summit seller economics.

Part III of this series is devoted entirely to the Middle Ring — the homes most likely to be underpriced today, and the listing strategy that captures the post-2016 value that the algorithms have not yet learned to see.

The Middle Ring is where Summit's biggest hidden seller premium lives. The 2016 rideshare program revalued these homes overnight — but most AVMs, and most listing agents, are still pricing them like it’s 2015.

Past the two-mile mark, the train station ceases to be the dominant pricing variable. The commute is no longer a short drive plus a $4 daily fee; it is a longer drive, a different decision matrix, and for many residents in this band, an entirely different commuting pattern — driving to a different station, driving into a closer hub like Maplewood or Millburn, or, increasingly, not commuting daily at all.

What replaces the transit premium in the Outer Ring is the topographical premium. This is the band where Summit's elevation gradient stops being a footnote and starts being the headline. Homes on the upper ridge of the Second Watchung Mountain — roughly 450 to 580 feet of elevation — carry viewshed, privacy, mature canopy, and prestige that the valley sections cannot replicate at any price. The buyer who is shopping in the upper Franklin Hill section at 1.9 miles from the train is not the same buyer who is shopping in the Edgewood area at 0.6 miles. They are different households, different income profiles, different commute patterns, often different stages of life.

The critical methodological point — and this is the central insight Part II of the series will develop — is that absolute elevation is the wrong variable. What capitalizes in the Outer Ring is viewshed, the actual geometric visibility from the parcel, accounting for tree canopy, neighboring rooflines, and the angle of sight. A home at 510 feet with an unobstructed western-facing line of sight over the Watchung Reservation is a fundamentally different asset than a home at 510 feet hemmed in by mature oaks on three sides. AVMs cannot see this distinction. Properly written listings can.

The Outer Ring seller's mistake is to lead with proximity to the station — which they do not have — rather than with the amenity they actually possess. The 1.4-mile homeowner can afford to lean on transit narrative. The 2.3-mile homeowner cannot. The pricing strategy at this distance is built on viewshed, lot prestige, architectural distinction, and a different commute story altogether.

The single most counterintuitive empirical feature of Summit's pricing landscape is that the bid-rent curve does not simply flatten as you move into the Outer Ring — it inverts. Past a certain distance from the station, and past a certain elevation threshold on the Watchung ridge, prices begin climbing again. The hedonic literature is unambiguous on this: buyers pay substantial, measurable premiums for elevation, viewshed, and the privacy that accompanies them. The premium does not erode the further you get from the train station; it competes with it.

This produces the inverse-correlation problem at the heart of every spatial econometric model of Summit. The properties with the highest transit accessibility (lowest network distance to the station) are, by physical necessity, the properties with the lowest elevation. The properties with the highest elevation — and by extension the most valuable viewsheds — are the properties farthest from the station. Two of the most powerful sources of housing value in this market sit on opposite ends of the same geographic axis.

For the seller, the practical implication is that the right comparable sales depend critically on which ring you are in. A 0.4-mile, 108-foot-elevation valley property cannot be reliably comped against a 2.1-mile, 540-foot-elevation ridge property even if their square footage, age, and lot size are identical. The buyers are not interchangeable. The asset bundles are not interchangeable. Treating them as equivalent is the most common — and most expensive — comp-selection error in the Summit market.

Two of the most powerful sources of housing value in Summit sit on opposite ends of the same geographic axis. The ridge competes with the train. The right comp set depends entirely on which side you’re on.

The remaining five posts in this series build out each piece of the framework in operational detail. For now, the scorecard below summarizes how the three rings differ — what capitalizes in each, what the buyer is actually paying for, and where the largest pricing errors tend to occur.

Identify your ring before you choose your comps. A great listing strategy in one ring is a malpractice-level mistake in another.

| Ring | Primary Premium | Lead With | Common Mispricing |

|---|---|---|---|

| I · Pedestrian 0 – 0.5 mi |

Walkable transit access; downtown amenity overlap | Network walk-time to platform; turnkey condition | Underpricing walkability; letting interior drag location |

| II · Middle 0.5 – 2.0 mi |

Post-2016 rideshare-enabled commute; full-house living | Generalized commute cost (Lyft + train); square footage and lot | Underpricing — AVMs still model pre-2016 friction |

| III · Outer > 2.0 mi |

Viewshed, elevation, privacy; architectural distinction | Line-of-sight, canopy, lot prestige — not the train | Leading with proximity to transit when the asset is elevation |

The single most important practical takeaway: identify your ring before you choose your comps. A great listing strategy in one ring is a malpractice-level mistake in another. The comp set that priced your neighbor's home correctly in 2018 may be the wrong comp set for your home in 2026, particularly if your home sits in the Middle Ring band that the rideshare program quietly revalued.

In Part II we turn to the Watchung viewshed problem in detail — what absolute elevation hides, why viewshed economics belong in a listing description, and how to document the line-of-sight evidence that actually moves a buyer's willingness to pay. From there, Parts III through VI walk through the Middle Ring revaluation, the Pedestrian Zone structural premiums, the AVM mispricing problem, and the synthesis pricing framework for sellers preparing to list.

Use network distance, not straight-line distance. Plot a walking route from your front door to the Summit Station platform — not the Google Maps driving distance. Under 0.5 miles by sidewalk is Ring One. Between 0.5 and 2.0 miles is Ring Two. Beyond 2.0 miles is Ring Three. Elevation matters as a secondary input, particularly for homes above 400 feet, where viewshed economics begin to dominate.

For Middle Ring homes specifically, yes. The pre-2016 parking constraint imposed a measurable discount on properties between 0.5 and 2.0 miles from the station because the commute was structurally unreliable. The Summit-Lyft partnership at 40 Railroad Avenue substituted operationally for a parking space. AVMs and many comp sets have not yet repriced this. Pedestrian Zone and Outer Ring sellers are less directly affected.

Automated valuation models assume a smooth, continuous price gradient and use comp sets selected primarily by proximity, square footage, and recency. They cannot detect the structural discontinuities at the 0.5-mile and 2.0-mile boundaries, they cannot read viewshed (only altitude, and often not even that), and they cannot retro-fit the 2016 rideshare inflection into their model. Part V of this series covers AVM mispricing in detail.

Neither is universally more valuable. They are two different amenities serving two different buyer profiles. The walkable downtown buyer is often a downsizer or transit-dependent professional and will pay a steep premium for Ring One. The ridge-section buyer values privacy, viewshed, and architectural prestige and will pay a steep premium for elevation with line-of-sight. Both premiums coexist. Neither erases the other.

Parts II through VI release over the coming weeks. Part II covers the Watchung viewshed problem and how to document line-of-sight for listing materials. Part III is the deep dive on the Middle Ring revaluation. Part IV covers the Pedestrian Zone. Part V is the AVM mispricing analysis. Part VI is the synthesis pricing framework for sellers.

A 30-minute pricing audit with The Prodigy Team covers your ring designation, comp-set selection, viewshed assessment, and a market-specific list-price recommendation grounded in the framework above.

Request Your AuditProdigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.