The unpaid renovation bill that can quietly attach itself to your house

When a contractor, subcontractor, or material supplier does work on your home and isn’t paid, New York’s Lien Law lets them file a mechanic’s lien against the property. It’s a powerful tool: once filed and recorded against your Staten Island home at the Richmond County Clerk, it clouds your title until it’s resolved.

The good news for homeowners is that the Lien Law treats single-family residences more protectively than commercial projects, with shorter deadlines and tighter renewal rules for the lienor.

This guide covers what a mechanic’s lien is, the special rules for single-family homes, and the three established ways to discharge one before it derails your closing.

Amechanic’s lien doesn’t require a lawsuit to attach — a contractor who believes they’re owed money can file one directly, and it lands on your title. That’s what makes it stressful. But the same Lien Law that lets them file also sets strict limits on timing and duration, and gives you clear, defined paths to get the lien off your property.

What a mechanic’s lien is

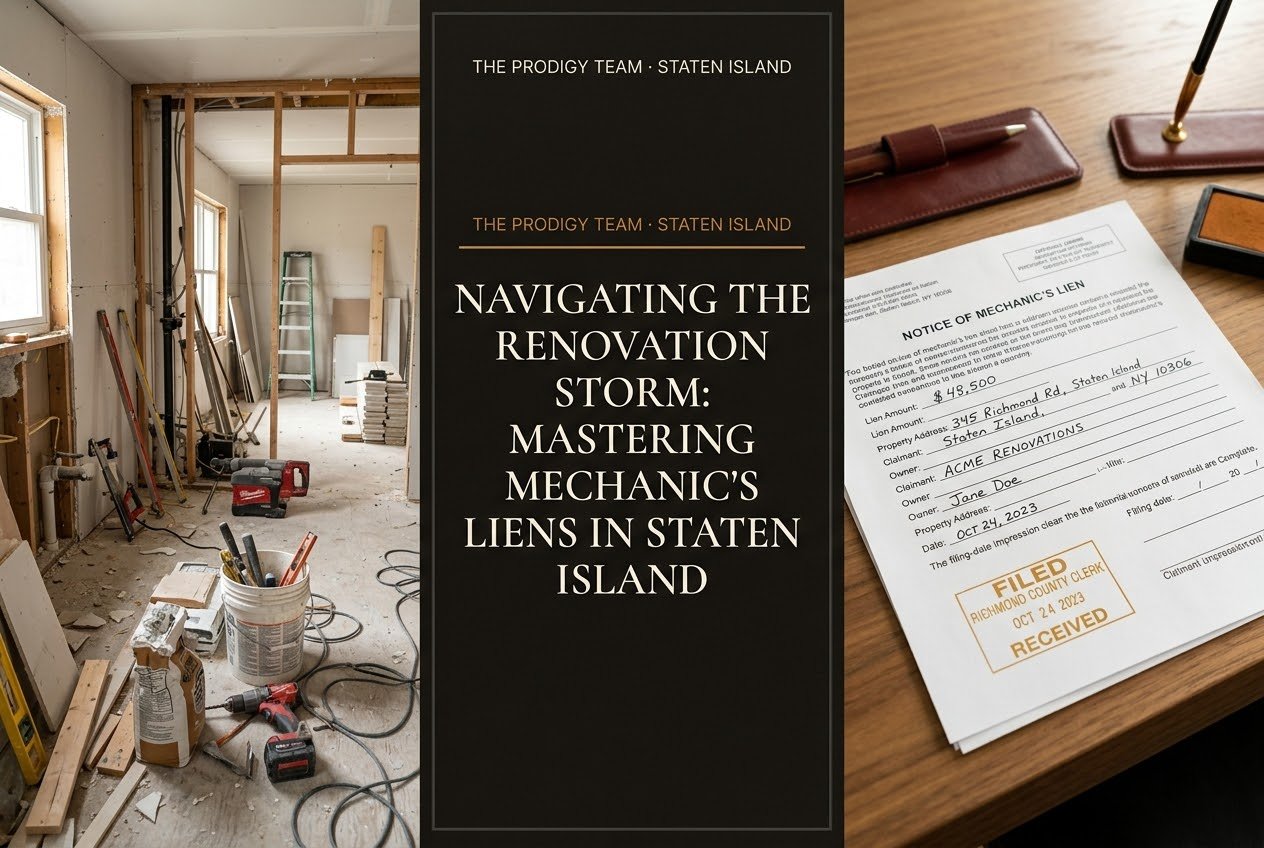

A mechanic’s lien is a claim filed under New York’s Lien Law by someone who provided labor or materials to improve real property and wasn’t paid — a general contractor, a subcontractor, or a material supplier. Filed and recorded against your home, it secures the alleged debt to the property itself, which means it has to be dealt with before clean title can pass to a buyer. On Staten Island the filing is made with the Richmond County Clerk, the same office that holds your deed and mortgage records.

Because Staten Island liens are recorded at the Richmond County Clerk rather than through ACRIS, a complete check for a mechanic’s lien means searching the County Clerk’s records or ordering a title search — not relying on the portal the other boroughs use.

The rules that favor single-family homeowners

The Lien Law distinguishes single-family homes from larger and commercial projects. For an existing single-family residence, the lien generally must be filed within four months after the last item of work or materials was furnished — a shorter window than the eight months allowed on commercial jobs. Once filed, a single-family residence lien is valid for one year. Critically, it can only be extended by a court order; a lienor cannot simply file an extension to keep it alive the way they can on commercial projects. If it isn’t extended or foreclosed within that year, it lapses.

Don’t treat the one-year clock as a reason to wait it out. A lienor can move to foreclose, and a lien sitting on your title blocks a sale right now regardless of when it would eventually expire. Waiting is not a strategy when you’re trying to close.

Three ways to clear it

New York gives you defined paths to discharge a mechanic’s lien. The first is payment: the debt is satisfied (or settled), and the lienor files a satisfaction discharging the lien. The second is bonding: you obtain a lien discharge bond, which substitutes the bond for the property as security and frees your title so the sale can proceed while the dispute continues. The third is depositing the lien amount with the court, which similarly discharges the lien against the real estate. Where the lien is defective or improperly filed, an attorney may also move to have it summarily discharged.

“If the debt is real, pay or settle it. If it’s disputed, bond it so the sale can close while the lawyers argue. Either way, the lien comes off the title — what you don’t do is let it sit there and hope the buyer’s attorney doesn’t notice.”

Your proactive game plan

If you’ve had renovation work done and there’s any unresolved dispute or unpaid balance, order a title search before listing so you know whether a lien has been filed. If one exists, get a real estate attorney involved early to choose between paying, settling, bonding, or challenging it. The earlier you act, the more options you have and the less leverage the timing gives the other side.

If a contractor relationship ended badly, run a title search now rather than assuming no news is good news. Finding a mechanic’s lien before you list lets you bond or settle it calmly instead of scrambling at closing.

A mechanic’s lien behaves like the judgment liens and tax liens in this series — all are recorded claims you clear before closing. The pre-listing self-audit walks through finding them.

Frequently asked questions

Can a contractor really put a lien on my house without suing me?

Yes. Under New York’s Lien Law a contractor, subcontractor, or supplier who provided labor or materials and wasn’t paid can file a mechanic’s lien directly against the property. No lawsuit or court judgment is required to file it, though foreclosing on it later does involve the courts.

How long does a mechanic’s lien last on a single-family home?

On a single-family residence the lien is valid for one year from filing and can only be extended by a court order — not by the lienor simply filing an extension. If it isn’t extended or foreclosed within that year, it lapses. The filing itself must occur within four months of the last work.

How do I remove a mechanic’s lien so I can sell?

There are three main paths: pay or settle the debt and obtain a satisfaction, post a lien discharge bond that substitutes for the property, or deposit the lien amount with the court. A defective or improperly filed lien can sometimes be discharged on motion by an attorney.

Should I just wait for the lien to expire?

Usually no. A lien on your title blocks a sale right now, the lienor can move to foreclose, and waiting surrenders your timing leverage. If you’re selling, it’s far better to pay, settle, or bond the lien so the deal can close.

Anthony Licciardello, Broker, The Prodigy Team

Anthony is a licensed real estate broker in New York and New Jersey and has run The Prodigy Team across Staten Island and New Jersey for more than 20 years. A former Director of Community Affairs in the Bloomberg administration and a member of the Staten Island Growth Management Task Force, he has spent his career on the land-use, zoning, and title issues that decide whether a Staten Island sale actually closes. Questions about your own property? Call 718-873-7345 or visit his agent profile.

Contractor dispute hanging over your home? Let’s make sure it doesn’t surface at closing.

We'll run a pre-listing title and building-file review so you head to market with a clean file and full leverage.

Why Sell With The Prodigy Team →Or call Anthony directly at 718-873-7345

This article provides general information for Staten Island homeowners and does not constitute legal, tax, or title advice. Laws, fees, and City programs change; verify current requirements with the relevant agency and consult a licensed attorney, tax professional, or title company about your specific property.