Anthony Licciardello | April 6, 2026

New Jersey Closing Costs

New Jersey consistently ranks among the most expensive states in the nation to close a residential real estate transaction. The average closing costs for buyers hover around 1.7% of the final sale price — but that number understates the real picture. Factor in mortgage origination fees, title insurance, municipal inspections, and attorney representation, and buyers in the $400,000 to $600,000 range routinely absorb $10,000 to $26,000 in settlement expenses before they get the keys.

Sellers have it harder. When real estate commissions are included alongside the state's Realty Transfer Fee, compliance certifications, and legal costs, sellers in New Jersey typically surrender 8% to 10% of their sale price at the closing table. On a home selling at the state's current median of approximately $535,000, that's $42,800 to $53,500 leaving the proceeds column before the seller sees a dollar.

Understanding New Jersey closing costs requires more than a national average. The state runs two distinct regional settlement models, taxes property transfers through a layered and recently overhauled fee structure, and delegates inspection requirements to 564 individual municipalities — each operating with its own rules, its own fee schedule, and its own pace.

02 — Seller Costs

The seller's cost burden in New Jersey is front-loaded by real estate commission, which averages 5.23% to 6% of the purchase price statewide. On a $535,000 sale, that single line item runs $27,980 to $32,100 before any government fees or administrative costs are applied. It is the largest check a seller writes at closing, by a wide margin.

Separate from commission, sellers bear several mandatory statutory and administrative expenses. The Realty Transfer Fee — a state-imposed tax on the seller covered in detail below — is the most significant governmental cost. Sellers are also responsible for obtaining municipal compliance documents: a Certificate of Occupancy or Certificate of Continued Occupancy, and in most towns, a fire safety inspection certification confirming the property meets minimum habitability and life-safety standards at transfer. Fees vary by municipality but typically range from $50 to $350 per certification.

Legal representation is standard practice statewide, with attorney fees running $1,500 to $3,000 depending on transaction complexity and geography. Sellers also pay to discharge any existing encumbrances — outstanding mortgages, tax liens, or municipal violations — from the public record. County recording fees for these discharges add $25 to $100 or more per document. Property taxes are credited or debited on a prorated basis, calculated to the exact day of closing.

For a granular breakdown of what selling specifically costs in one Union County market, the Westfield seller closing cost guide walks through every line item in detail.

| Seller Cost | Typical Range |

|---|---|

| Real Estate Commission | 5.23% – 6.00% of purchase price |

| Realty Transfer Fee (RTF) | Scaled by purchase price tier — see below |

| Graduated Percent Fee (GPF) | 1.0% – 3.5% on sales over $1,000,000 |

| Attorney / Legal Fees | $1,500 – $3,000 |

| Municipal CO & Fire Certifications | $50 – $350 per certification |

| Title Search (Seller Side) | $150 – $500 |

| Recording Discharge Fees | $25 – $100+ per document |

| Prorated Property Taxes | Calculated to exact closing date |

03 — Buyer Costs

Buyer closing costs in New Jersey typically land between 2% and 5% of the purchase price. The range reflects one critical variable: whether the buyer is financing or paying cash. Financed buyers absorb the full stack of lender-mandated fees; cash buyers bypass them entirely and can compress total settlement costs to roughly 1% to 2% of the purchase price — consisting primarily of title insurance, legal fees, and government recording charges.

For financed buyers, mortgage-related costs form the largest cluster. Lenders charge origination fees of 0.5% to 1% of the loan amount, translating to $1,000 to $4,000 on a typical mid-tier purchase. Underwriting fees, credit check charges ($25 to $75), a mandatory appraisal ($300 to $600), and initial escrow funding to prefill reserves for property taxes and homeowner's insurance add on top of that. Rate lock fees may apply depending on the lender and market conditions at time of application.

Due diligence costs fall entirely on the buyer. A standard home inspection runs $300 to $600; termite and pest inspection adds $75 to $400. A property survey — required for most title policies and lender commitments — ranges from $500 to $2,000 depending on lot size and boundary complexity. Buyers are also customarily responsible for both the lender's title insurance policy and the optional but strongly advisable owner's title insurance policy, combined running $800 to $2,000. Attorney fees on the buyer side run $1,200 to $2,500 in North Jersey markets where representation is standard.

One line item frequently overlooked: buyers purchasing into a condominium association, homeowners association, or co-op are typically assessed a one-time capital contribution at closing — usually one to three months of monthly dues — deposited into the association's reserve fund for future major repairs. Non-refundable, and it can run from a few hundred dollars to several thousand in larger communities.

Cash buyers in New Jersey can cut their total closing costs nearly in half — eliminating lender fees, appraisal requirements, and escrow prefunding compresses the settlement burden to roughly 1% to 2% of the purchase price.

| Buyer Cost | Typical Range |

|---|---|

| Loan Origination & Underwriting | 0.5% – 1.0% of loan amount ($1,000 – $4,000) |

| Appraisal Fee | $300 – $600 |

| Title Insurance (Lender & Owner) | $800 – $2,000 |

| Home & Termite Inspections | $375 – $1,000 combined |

| Property Survey | $500 – $2,000 |

| Attorney / Legal Fees | $1,200 – $2,500 |

| Recording Fees (Deed & Mortgage) | $100 – $300+ |

| Prepaid Taxes & Insurance (Escrow) | 2 – 3 months' reserves, varies by tax rate |

| HOA / Condo Capital Contribution | 1 – 3 months of dues, where applicable |

04 — Regional Customs

New Jersey is one of the few states where your closing experience — and your projected legal costs — depend significantly on which county the property sits in. The state operates under two distinct regional settlement models, and the divide runs roughly through the center of the state.

In the northern counties — Bergen, Essex, Hudson, Morris, Passaic, Sussex, and Union — both the buyer and seller are expected to retain independent legal counsel. Attorneys don't just review contracts; they act as the primary settlement agents, coordinating the title search, managing lender communications, preparing closing disclosures, and handling fund disbursement. This framework provides meaningful legal protection during the mandatory three-day attorney review period that follows any signed contract, and during inspection contingency resolution and title defect negotiation. The cost is real: legal fees in North Jersey run $1,200 to $3,000 per side, and both parties pay.

The southern and central counties — Atlantic, Burlington, Camden, Cape May, Cumberland, Gloucester, and Salem — operate closer to the national norm. Title companies serve as the neutral settlement agent, handling title examination, document preparation, and fund disbursement. Independent attorney representation is an option, not an expectation. Settlement service fees from a title agency typically run $300 to $900, meaningfully lower than the attorney fees they replace in the north.

One constant across both models: title insurance premiums in New Jersey are regulated by the Department of Banking and Insurance under N.J.S.A. 17:46B-1, meaning the cost of a title policy is identical regardless of which agency issues it. The standard conveyance instrument statewide is the Bargain and Sale Deed with covenants against the grantor's acts.

Attorney-driven. Both sides retain independent counsel. Legal fees $1,200–$3,000 per party. Attorneys act as primary settlement agents through closing.

Title company-driven. Agency handles settlement and disbursement. Attorney representation optional. Settlement fee $300–$900.

Title insurance rates regulated uniformly by DOBI. Bargain and Sale Deed is the standard conveyance instrument across all 21 counties.

05 — State Taxation

The Realty Transfer Fee is a mandatory, seller-paid tax levied on every transfer of real property in New Jersey. There is no exception for hardship or circumstance: the county clerk will not record a deed unless the RTF has been paid in full. Revenue flows to the state's general fund, neighborhood revitalization programs, and shore protection initiatives, distributed between the state and the county where the property sits.

The RTF calculation is more complex than most sellers expect. The structure is tiered and incremental — but the rate schedule resets entirely based on whether the total consideration is above or below $350,000. Cross that threshold and the entire calculation restarts at steeper rates from the first dollar. It is not a marginal increase; it is a full structural shift applied to the whole consideration.

For sales where the total consideration does not exceed $350,000, the fee is calculated incrementally across three brackets:

| Consideration Tier — Under $350,000 | Rate per $500 of Consideration |

|---|---|

| $0 – $150,000 | $2.00 |

| $150,001 – $200,000 | $3.35 |

| $200,001 – $350,000 | $3.90 |

If the total consideration exceeds $350,000, the rate schedule resets and applies from the first dollar at meaningfully higher rates:

| Consideration Tier — Over $350,000 | Rate per $500 of Consideration |

|---|---|

| $0 – $150,000 | $2.90 |

| $150,001 – $200,000 | $4.25 |

| $200,001 – $550,000 | $4.80 |

| $550,001 – $850,000 | $5.30 |

| $850,001 – $1,000,000 | $5.80 |

| Over $1,000,000 | $6.05 |

Three seller categories receive meaningful relief on the RTF. Qualifying senior citizens aged 62 or older, blind persons, and disabled persons are eligible for significantly compressed rates across all tiers. Transfers between spouses and between parents and children are fully exempt from the RTF — no fee applies regardless of the purchase price. One important distinction: these RTF exemptions do not carry over to the Graduated Percent Fee. The GPF has no provision for senior, disability, or veteran discounts of any kind. Always confirm current RTF rates with the NJ Division of Taxation or through your attorney before closing.

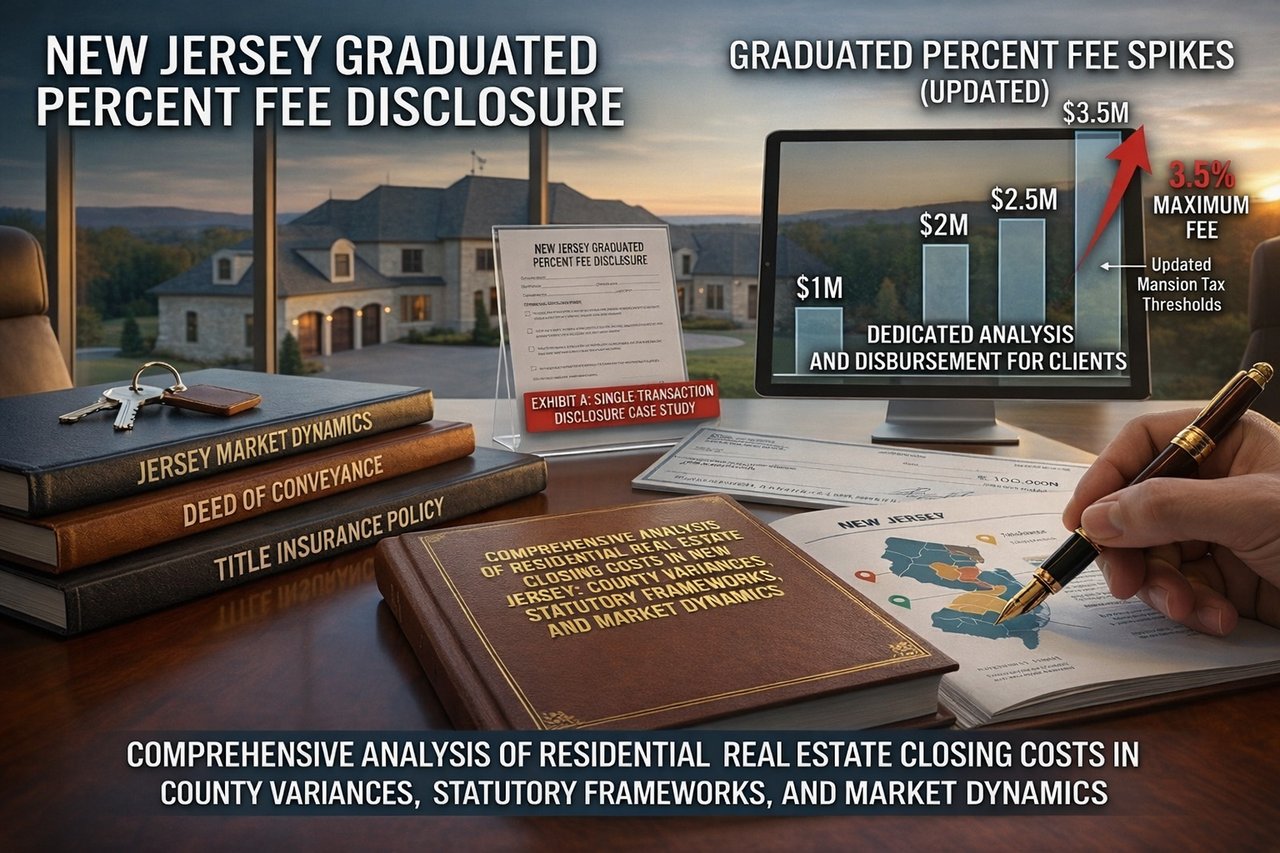

06 — GPF Overhaul

Prior to July 10, 2025, New Jersey imposed a 1% "Mansion Tax" on the buyer for any residential property transfer over $1,000,000. That flat 1% applied to the entire purchase price — not just the amount above the threshold — meaning a $1,050,000 purchase generated an immediate $10,500 tax liability for the incoming buyer.

Governor Phil Murphy signed legislation that permanently eliminated the buyer-side Mansion Tax effective July 10, 2025. In its place, the state enacted the Graduated Percent Fee — a replacement tax shifted entirely onto the seller, assessed on top of the standard RTF, with a far more aggressive tiered structure.

The mechanics create catastrophic pricing cliffs. The GPF is a flat tax applied to the entire consideration once a tier is crossed — not a marginal tax on only the overage. The real-dollar math illustrates the problem directly:

One dollar above a GPF threshold can cost a seller more than $20,000. In Bergen, Morris, Somerset, and Monmouth — where luxury pricing decisions happen daily — running the tax math at every scenario above $1,000,000 is now a non-negotiable part of the listing conversation.

In Monmouth County markets where estate sales and precision luxury pricing already define the segment, the GPF tiers require listing agents and sellers to run explicit tax-impact calculations at every price point above $1,000,000. The difference between listing at $1,980,000 and $2,050,000 is no longer just a marketing decision — it's a $21,000 tax decision. Pricing strategy in the NJ luxury market was already competitive. The GPF added a mandatory analytical layer that did not exist before July 2025.

For how pricing velocity and seller strategy are playing out in an active Monmouth County market, the Red Bank market data report covers current transaction dynamics in detail.

07 — Recording Fees

Once a transaction closes, the deed, mortgage, and any discharge documents must be officially recorded with the County Clerk. Base recording fees are relatively uniform across New Jersey's 21 counties: recording a deed costs $40 to $45 for the first page — which includes a mandatory $10 tax abstract fee — plus $10 for each additional page. Recording a standard mortgage costs $30 to $35 for the first page, plus $10 per subsequent page.

Beyond the base fees, the County Homelessness Trust Fund Act (P.L. 2009, c. 123) authorizes county governments to levy a surcharge on every document recorded by the County Clerk. Because a standard closing involves recording multiple instruments — at minimum the deed, the new mortgage, and any prior mortgage discharge — this surcharge compounds across the document stack. The rate runs $3 to $5 per document depending on county, and four counties have opted out entirely.

| Surcharge per Document | Counties |

|---|---|

| $3.00 | Camden, Essex, Mercer, Somerset |

| $5.00 | Atlantic, Bergen, Burlington, Cape May, Cumberland, Gloucester, Hudson, Middlesex, Monmouth,* Ocean, Passaic, Salem, Union |

| None | Hunterdon, Morris, Sussex, Warren |

*Confirm Monmouth County surcharge status with the Monmouth County Clerk at time of transaction.

Individual county clerks also impose unique fees for specialized document types. Bergen County charges $40 to file a Lis Pendens and $25 for a UCC-1 Financing Statement. Union County charges $15 for inheritance tax waivers. Middlesex County charges $20 to $40 for a Notice of Settlement depending on the number of parties involved. Cape May County adds $6 per additional name beginning with the sixth party indexed on any document. Always request the current fee schedule from the applicable county clerk before projecting total recording costs.

In 2026, the legislature extended this framework by authorizing individual municipalities to establish their own Homelessness Trust Funds via an additional fee of up to $5 on building permits and certain existing local fees. Recording-adjacent costs are likely to increase incrementally as more municipalities opt in.

08 — Municipal Compliance

New Jersey's tradition of home rule means each of its 564 municipalities sets its own prerequisites for a legal property transfer. Before a closing can proceed, the seller must generally obtain either a Certificate of Occupancy or a Certificate of Continued Occupancy confirming the property meets local habitability standards — and in most municipalities, a separate fire safety certification as well.

Under the state's Uniform Fire Code (N.J.A.C. 5:70-2.9), every one- and two-family dwelling must pass a physical inspection by the local fire prevention bureau before any change of occupancy. Inspectors verify functioning smoke detectors on every level, carbon monoxide alarms outside each sleeping area, and an appropriate kitchen fire extinguisher. Fees vary dramatically by town — some municipalities charge $50 to $100 for the inspection, others run $200 to $350, and several impose reinspection fees that can double the total cost if the property fails the initial visit.

The deeper issue is scheduling. Many municipal inspection offices operate limited hours and carry multi-week backlogs, particularly in spring and summer when transaction volume peaks. Sellers who wait until after contract execution to schedule these inspections frequently delay their own closings. Experienced listing agents in NJ typically recommend initiating the CO and fire inspection applications at the same time the property is listed — not after a contract is signed.

An additional layer applies to investors and landlords. Legislation effective July 2022 mandates lead-based paint inspections — including wipe tests — on one-to-four-unit rental properties built before 1978 whenever a CO is issued or tenant turnover occurs. If lead is detected, the property owner must complete abatement or encapsulation before the transaction can clear. For pre-1978 housing stock in Bergen, Essex, Hudson, and Union counties, this represents a material latent closing cost that many sellers do not anticipate until it surfaces during the inspection process.

Closing costs in New Jersey do not exist in isolation from these variables. The final settlement figure for any specific transaction is determined by the county, the municipality, the financing structure, the sale price tier, and the property's age and condition. The ranges outlined above provide the structural framework — but the actual numbers assemble line by line at the closing table.

FAQ

Who pays closing costs in New Jersey — the buyer or the seller?

Both parties pay closing costs, but the seller's total burden is significantly larger. Sellers typically pay 8% to 10% of the purchase price when commissions and state transfer taxes are included. Buyers typically pay 2% to 5%, with the range driven primarily by whether the purchase is financed or cash — cash buyers eliminate the lender-mandated fee stack and can settle for 1% to 2% of the price.

What is the Graduated Percent Fee in New Jersey and who pays it?

The Graduated Percent Fee replaced the former buyer-side Mansion Tax effective July 10, 2025. It is now paid by the seller on all residential transfers over $1,000,000, and it is assessed on the entire sale price — not just the amount above the threshold. The rate scales from 1% on sales between $1,000,000 and $2,000,000 up to 3.5% on sales above $3,500,000, creating hard pricing cliffs where crossing a tier boundary can add tens of thousands of dollars in tax liability.

Do you need a real estate attorney to close on a house in New Jersey?

In northern New Jersey counties — Bergen, Essex, Hudson, Morris, Passaic, Sussex, and Union — attorney representation is standard practice for both buyers and sellers and is widely expected by market participants. In southern counties, title companies typically handle settlement and attorney representation is optional. All parties statewide have the legal right to retain counsel, and in any transaction with complexity — title issues, inspection disputes, or estate-involved transfers — doing so is advisable regardless of county.

What is a Certificate of Occupancy and why does it affect my closing in NJ?

A Certificate of Occupancy is a municipal document confirming the property meets local habitability and building code standards at the time of transfer. Most of New Jersey's 564 municipalities require this certificate and a separate fire safety inspection before a closing can legally proceed. Because each municipality sets its own fees and inspection capacity, sellers should initiate the application as early as possible — ideally when the property goes on market — to avoid delays at the closing table.

Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.