Anthony Licciardello | June 3, 2026

Lavalette, NJ

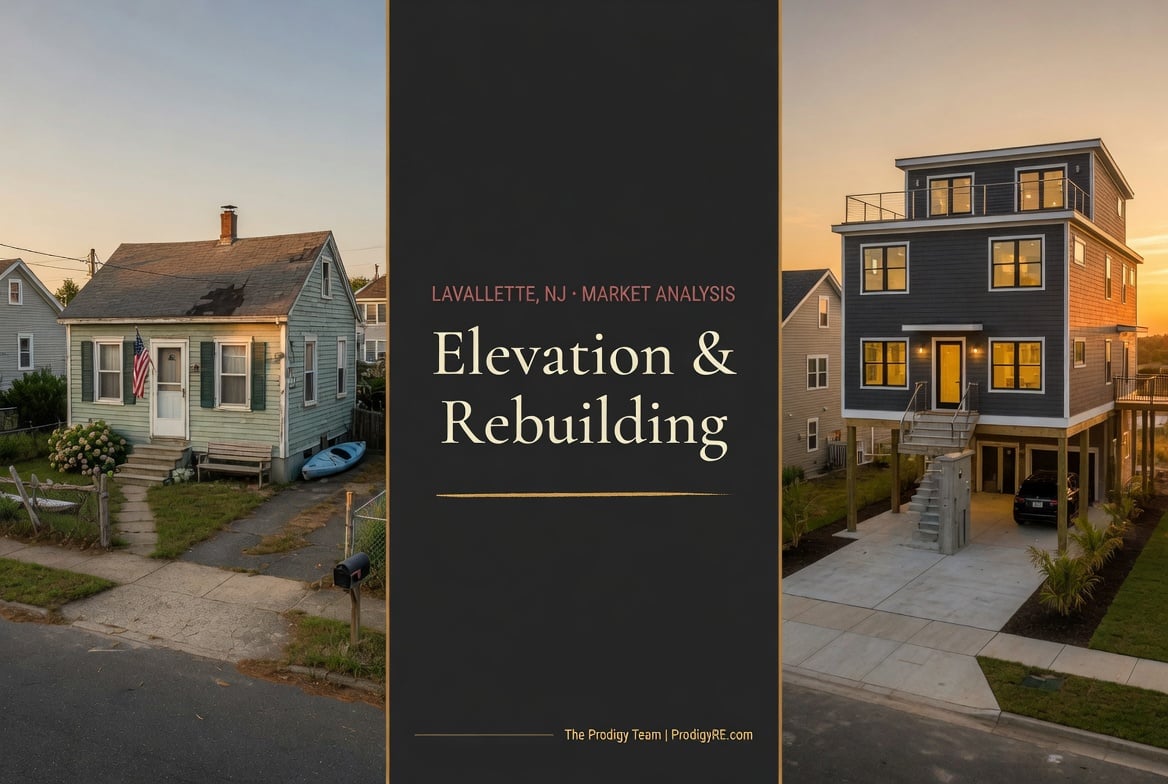

Walk the island and you’ll see two housing stocks side by side: low older cottages and tall new homes on pilings. That contrast is the story of Lavallette since Sandy — and it shapes what you should buy, renovate, or rebuild.

Why are so many Lavallette homes raised up on pilings?

Because after Superstorm Sandy, FEMA and NFIP rules required homes that were substantially damaged — or substantially improved (renovations of 50% or more of value) — to be elevated to or above current Base Flood Elevation. Elevating also sharply lowers flood-insurance costs. The result is a wave of new and rebuilt homes lifted on pilings, standing beside the lower older cottages that predate the rules.

No single event shaped today’s Lavallette housing stock more than Superstorm Sandy in 2012. The storm and the rules that followed didn’t just repair the island — they raised it, replacing or lifting a large share of its homes and creating the two-tier landscape you see now: older low-set cottages beside taller, elevated new construction. For anyone buying, renovating, or rebuilding here, understanding that dynamic isn’t history — it’s the framework for the most consequential and expensive decisions you’ll make.

When Sandy struck the Barnegat Peninsula in October 2012, it inflicted severe flood and surge damage across Lavallette. In the rebuilding that followed, two forces converged: FEMA updated and generally raised the flood maps and Base Flood Elevations for coastal New Jersey, and the rules governing damaged and rebuilt homes required them to be reconstructed to those higher standards. Owners rebuilding weren’t putting back what was lost — they were building higher.

The visible result is the island’s defining architectural signature today: homes lifted on pilings, with living space well above grade and parking or storage tucked underneath. Alongside them remain the older, lower cottages that survived or predate the changes. That coexistence — old-and-low next to new-and-high — is exactly the contrast a buyer needs to read, because the two carry very different costs, risks, and futures.

Two related triggers decide when a home must be elevated, both from the National Flood Insurance Program. The first is substantial damage: if a building is damaged such that restoring it would cost 50% or more of its pre-damage market value, it must be rebuilt to current standards — which on this island means meeting or exceeding the current Base Flood Elevation. This is the rule that forced so much elevation after Sandy.

The second is substantial improvement: the same 50%-of-value threshold applies to voluntary work. If your planned renovation, addition, or reconstruction reaches or exceeds half the building’s market value, the whole structure must be brought up to code — including elevation. This is the rule that catches buyers who purchase a low, older cottage planning a big renovation, only to discover the project legally requires lifting the entire house.

The 50% threshold is measured against the building’s value, not the property’s — and on the shore, where land is much of the value, that building number can be lower than you’d expect. A renovation that feels modest relative to the purchase price can still cross 50% of the structure’s value and trigger full elevation. Confirm the building valuation and the threshold with the Borough before you scope a major renovation.

Once elevation is on the table, owners of older homes face a fork. Elevating an existing home — lifting the structure onto new pilings or a raised foundation — preserves a sound house while bringing it into compliance and cutting insurance costs. It can be the right call for a structurally solid home with good bones. Tearing down and rebuilding makes more sense when the existing home is dated, too small for the lot’s potential, or not worth the cost and disruption of lifting — especially where land value dominates and the highest use of the parcel is a larger, modern, elevated home.

The economics echo the teardown logic of high-value mainland towns, but with a coastal twist: here, elevation isn’t optional once a trigger is hit, so the comparison isn’t “renovate as-is vs. rebuild” but “elevate-and-renovate vs. rebuild elevated.” On many desirable Lavallette lots, builders and buyers increasingly choose the rebuild, which is why new elevated construction keeps replacing the older stock.

The question I ask first about an older Lavallette home isn’t “what does it need” — it’s “does the renovation cross 50%, and if it does, what does elevating cost?” That single answer often decides renovate-vs-rebuild before any design conversation starts. Buyers who learn it early save themselves from sinking money into a plan the rules won’t allow as drawn.

If you’re buying, the elevation question reframes how you value the two housing stocks. A newer elevated home costs more upfront but comes with compliance handled, lower flood-insurance costs, and modern construction — you’re buying the solution. An older lower home may look like a value, but price in the real possibility that any significant renovation triggers elevation, and that its flood insurance runs higher in the meantime. The cheaper sticker can be the more expensive project.

The practical move: if you’re considering an older home with renovation in mind, get a realistic renovation estimate, the building’s value, and an elevation-cost estimate before you commit — so you know whether you’re buying a quick refresh or a lift-the-whole-house project. Either can be a good buy; only one of them is the one you think you’re making if you skip the diligence.

The flood-zone and insurance mechanics behind all of this are covered in the dedicated flood guide.

If you own an older, lower home, the elevation dynamic shapes your sale. Your most likely buyer may well be someone — a builder or a buyer-with-builder — who intends to elevate or rebuild, which means heavy cosmetic renovation before listing can be wasted money, much like the teardown calculus on the mainland. Understanding whether your home is a candidate for elevation or a full rebuild tells you which buyer to market to, and whether to spend on updates at all.

If you own a newer elevated home, that compliance and lower insurance cost is a genuine selling point — make it explicit in the marketing, because buyers who understand the island will pay for not having to solve the elevation problem themselves. In both cases, pricing correctly means reading where your specific home sits in the old-vs-elevated spectrum and who will pay the most for it.

For the full market picture, see the complete Lavallette real estate guide; for the buyer’s cost framework, the shore-home buying playbook.

When do I have to elevate a Lavallette home?

When it’s substantially damaged (repairs of 50%+ of building value) or substantially improved (renovations of 50%+ of building value). Either triggers a requirement to rebuild to current standards, which on this island means elevating to or above Base Flood Elevation. Confirm specifics with the Borough.

Is it better to elevate an old home or tear it down?

It depends on the home and lot. Elevating preserves a structurally sound house and brings it into compliance; tearing down makes sense for dated or undersized homes, especially where land value dominates and a larger modern elevated home is the highest use. Compare the full cost of each before deciding.

Does elevating a home lower flood insurance?

Generally yes, often substantially. Flood premiums are tied closely to the lowest floor’s height relative to Base Flood Elevation, so raising a home above BFE typically reduces the premium — one of the main financial reasons owners elevate beyond the legal requirement.

Should I buy an older or a newer elevated home in Lavallette?

A newer elevated home costs more but has compliance handled and lower insurance; an older lower home can be a value but may trigger elevation if you renovate heavily and costs more to insure meanwhile. Get renovation and elevation estimates before buying an older home to improve.

This article is informational and not legal, engineering, or construction advice. Flood maps, Base Flood Elevations, the substantial-damage/improvement rules, and local building requirements are property-specific and change over time. Confirm current requirements with the Borough of Lavallette construction and flood plain officials, and consult licensed professionals before renovating or rebuilding.

Anthony Licciardello

Broker of The Prodigy Team and a licensed real estate broker in New Jersey and New York, serving Ocean County and the Jersey Shore. A former Director of Community Affairs in the Bloomberg Administration and member of the Staten Island Growth Management Task Force, Anthony brings a land-use–aware lens to elevation, rebuilding, and new-construction decisions on the barrier island. 718-873-7345

Know the real cost of lifting it — before you buy or renovate.

The Prodigy Team reads elevation, the 50% rule, and rebuild economics into every Lavallette valuation — and our buyer pipeline connects the right buyers, builders, and sellers to the right island lots.

Get Your Shore Home Valuation →Prodigy Real Estate is an innovative real estate company offering high-end video production, home valuation services, purchasing, and home sales. Serving New York and New Jersey.